This has been a strange season for Liverpool. On the one hand, they have won their first trophy since 2006 by beating Cardiff City to secure the Carling Cup, which guarantees them European football next season, and have the chance of more silverware, having reached the FA Cup final. On the other hand, their form in the Premier League has been disappointing to say the least and they currently lie in eighth place, which is far below the expectations of their fans.

It is therefore difficult to work out whether the club is moving in the right direction, though there is little doubt that their new owners would have expected more from the Reds. Before the season commenced, John W Henry spoke about their objectives, “It’s too early for us to talk about winning the league. Our main goal is to qualify for the Champions League. If we don’t, it would be a major disappointment.”

That’s a pretty clear statement of intent, which was re-iterated by managing director Tom Werner, who described the Carling Cup success as “a big day for us”, but immediately emphasised that “our goal is still to reach the Champions League.” In other words, winning a domestic cup is fine, but success is defined by “finishing in the top four.” Of course, the focus on the league should be nothing new to Liverpool fans, as this was a mantra of the legendary Bill Shankly, “The league is a marathon not a sprint. It is where you find out if you are entitled to believe in how good you are.”

"John W Henry & Tom Werner - Magic Moments"

It was not meant to be this way. The returning Kenny Dalglish had worked wonders last season, bringing back the feel good factor and more importantly delivering results on the pitch. Hopes were high that Liverpool’s combination of old managerial skills and new money would produce a return to former glories, but the project is still very much a work in progress.

Dalglish has done himself few favours with some combative media interviews, though an irascible Scottish manager has not exactly hurt Manchester United. More importantly, Liverpool’s season has been de-railed by injuries to key players, such as Steven Gerrard, Daniel Agger and (crucially) the previously unheralded Lucas Leiva, plus the absence through disciplinary reasons of Luis Suarez. Even so, the Reds would have been higher in the table if they could have finished the numerous chances they created, thus converting draws into wins and avoiding so many one-goal defeats.

Of course, most teams could make the same excuses, but it is compounded in Liverpool’s case by the large amount of money they have spent on bringing in new players, which should have addressed some of the obvious weaknesses in the squad, such as finding someone able to consistently put the ball in the net. The policy of buying British has not exactly been a glittering success to date, exacerbated by the high fees spent on the likes of Andy Carroll, Stewart Downing, Jordan Henderson and Charlie Adam.

"Stevie wonders"

Although the side has under-performed, at least the owners’ willingness to back the manager in the transfer market should be applauded (“a significant commitment”, according to managing director Ian Ayre), especially as this is in stark contrast to the parsimonious approach adopted by their reviled predecessors, Tom Hicks and George Gillett. There seems to be an element here of proving to the fans that the new boss is not like the old boss, as Henry observed, “There was a fear we wouldn’t spend.” More positively, Billy Hogan, managing director of Fenway Sports Marketing, outlined the group’s philosophy, “You’re seeing the desire to win and the desire to compete in the transfer market.”

It’s worth pausing to reflect on how different this is from the unpopular former owners, who saddled Liverpool with a mountain of debt when they bought the club in March 2007, then took them to the brink of administration. The desperate situation was crisply summarised by UEFA’s William Gaillard: “The club has been rescued, thank God, but it was a close call. They suddenly found themselves being owned by two failed banks that had been taken over by governments.”

Liverpool’s debt had reached shocking levels under the previous unwanted regime. Although there was “only” £123 million net debt in the football club, the full picture was revealed in the holding company where borrowings had grown to around £400 million. The good news is that this debt was largely eliminated after the change in ownership, though there is still £65m net debt, comprising £38 million bank loans and £30 million owed to UKSV Holdings less £3 million cash.

This is enormously significant to the club’s finances, as the prohibitively expensive annual interest payments of £18 million (£40 million including the holding company) have been drastically reduced to just £3 million, which Ayre said meant that Liverpool are “in a much stronger position to utilise our revenues more effectively on the team.”

This is enormously significant to the club’s finances, as the prohibitively expensive annual interest payments of £18 million (£40 million including the holding company) have been drastically reduced to just £3 million, which Ayre said meant that Liverpool are “in a much stronger position to utilise our revenues more effectively on the team.”

However difficult this season is proving, there is no doubt that it is preferable to the depths of despair suffered under the previous “gang of four”: Hicks and Gillett, a couple of charmless chancers; Christian Purslow, a smug, superficial excuse of a chief executive, who delivered little beyond infamously nominating himself as “the Fernando Torres of finance”; and poor Roy Hodgson, an experienced manager who was the archetypal square peg in a round hole (though apparently good enough to lead his country).

The arrival of Fenway Sports Group (FSG) has dramatically improved the club’s finances, as noted by Dalglish, “Off the pitch, especially, the club is a lot stronger than it was… see how much money we are getting through sponsorship and kit deals.” This comment was widely ridiculed, but he does have a point: the use of the money may be open to question, but at least it’s now available.

Some may wish that the owners would provide even more financing, but this is infinitely better than recent years when top class players were sold and replaced by inferior “talents” – Christian Poulsen and Joe Cole for Xabi Alonso and Javier Mascherano, anyone?

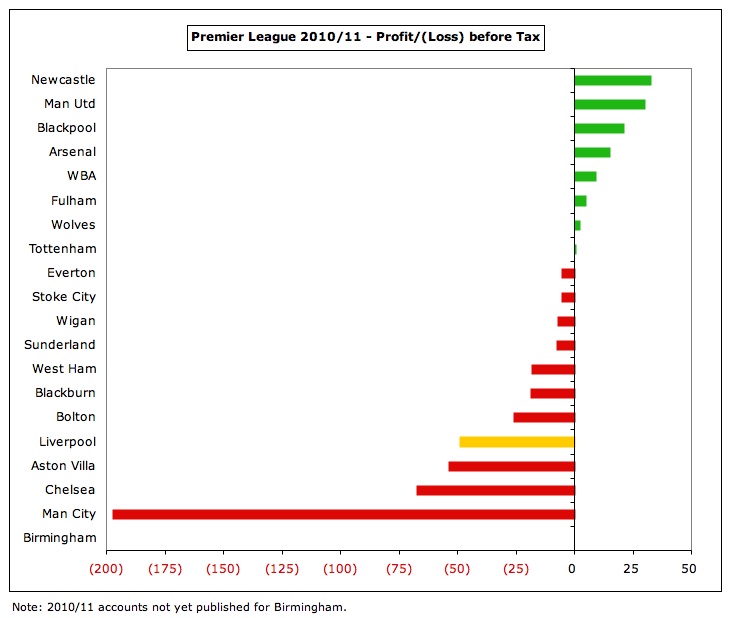

On the face of it, this improvement has not yet been reflected in the figures, as Liverpool announced a £49.3 million loss before tax for 2010/11, £29 million worse than the previous year, though much of this was due to clearing up the mess left by the “cowboys” with the club booking enormous exceptional expenses of £59m, mainly £49.6 million relating to the aborted stadium plans and £8.4 million termination payments to Hodgson (and his backroom staff) plus Purslow.

This is fairly typical of new management coming in and cleaning house. As Ayre said, “It is a big loss and a big write-off, but it means that it’s gone forever now and we can move forward without that around our neck.”

Excluding exceptional expenses, Liverpool would actually have made a profit of around £10 million, but the worrying thing is that this was only after hefty profits on player sales of £43 million, largely Fernando Torres to Chelsea and Javier Mascherano to Barcelona. If both once-off items are excluded, the underlying loss is around £34 million, similar to the previous year.

Although EBITDA (Earnings Before Interest, Taxation, Depreciation and Amortisation) is positive at £10 million, it has declined for the second year in succession and is on the low side, e.g. Manchester United’s is £111 million. After taking into consideration depreciation and player amortisation (an important part of any football club’s business), Liverpool’s operating loss excluding exceptionals was £31 million.

In fact, Liverpool have consistently been making losses with only one profit reported in the football club in the last six years (2008, boosted by large player sales). Losses were even higher at the holding company level, after including all interest payable, amounting to a shocking £178 million in the four years before Hicks and Gillette exited stage left (2007 £33 million, 2008 £41 million, 2009 £55 million and 2010 £49 million).

The Reds also have to pull their socks up if we consider that many other teams are improving their financial performance. In 2009/10 only four clubs in the Premier League made a profit, but this doubled to eight in 2010/11 with many maintaining solid finances while performing well on the pitch, e.g. Manchester United, Arsenal, Tottenham and Newcastle United. On the other hand, there are still clubs registering large losses in their pursuit of honours, notably Manchester City £197 million and Chelsea £67 million.

Where Liverpool have done well is to hold their revenue at about the same level following the £21 million reduction due to the failure to qualify for the Champions League. They compensated this with a £7 million increase in the Premier League distribution, thanks to the improved central deal, and a striking £15 million increase in commercial income.

Uniquely among leading English clubs, the highest proportion of Liverpool’s revenue comes from their commercial arm with 42%. In fact, this has been the main driver of the club’s revenue growth, contributing £40 million (63%) of the £64 million rise in the last five years.

Even so, the operating loss widened following a £15 million increase in the wage bill, which grew 13% from £114 million to £129 million (excluding termination payments), meaning that the important wages to turnover ratio increased from 62% to 70%. This is much worse than Manchester United 46%, Arsenal 55% and Spurs 56%, but considerably better than Manchester City 114%.

Player amortisation, the annual cost writing-off transfer fees, fell to £36 million, though it is likely to rise after last summer’s acquisitions, although will again be far behind Manchester City’s £84 million.

All in all, Liverpool should really be doing better with the resources at their disposal, both in terms of their revenue and wage bill.

Even with the slight decrease in revenue to £184 million, their revenue is still comfortably the fourth highest in England, £20 million ahead of Tottenham, £30 million more than Manchester City and around twice as much as Aston Villa, Newcastle and Everton. On the other hand, they remain handicapped compare to the top three revenue generators, more than £40 million less than Arsenal and Chelsea (both around £225 million) and an incredible £150 million behind traditional rivals Manchester United (£331 million). That’s a significant competitive disadvantage.

Nevertheless, Liverpool are in a more than respectable ninth place in Deloitte’s European Money League, which is not to be sneezed at, especially as they are the only club in the top ten that did not compete in the Champions League in 2010/11. More gloomily, the Spanish giants continue to surge ahead with Real Madrid and Barcelona earning £433 million and £407 million respectively. That £200-250 million shortfall could either be considered an insurmountable obstacle or something to target, especially the commercial revenue, which is around double Liverpool’s.

It’s a similar story with the wage bill of £129 million, which is the fourth highest in the Premier League, a little higher than Arsenal (£124 million), but a fair way ahead of the next club Tottenham (£91 million) and perhaps more pertinently over twice as much as Newcastle (£54 million). However, it is a lot lower than Manchester United (£153 million), Chelsea (£168 million) and new kids on the block Manchester City (£174 million).

That said, Liverpool have been faced with escalating financial challenges over the last few years, both externally and internally.

On the external side, there has been a clear increase in competition, as the “Big Four” has expanded into the “Sky Six” with the addition of Manchester City and Tottenham, who have both managed to break the glass ceiling of Champions League qualification. City have been backed by Sheikh Mansour’s billions, while Spurs have benefited from the astute business guidance of Daniel Levy.

This can be seen by looking at the revenue trend of those clubs, which shows that Liverpool is the only one to have negative revenue growth since 2009. In the same period, the two Manchester clubs and Tottenham have all grown their revenue by more than £50 million. Arsenal’s revenue was also flat, but they are now £43 million ahead of Liverpool, having been £7 million behind in 2005 (a £50 million turnaround).

Furthermore, some of those clubs have spent big in their pursuit of success, notably Manchester City and Chelsea. As Henry said when asked what surprised him most about football, “The sums of money that are spent on buying and selling players is remarkable.”

Everyone bangs on about Liverpool’s activity in the transfer market since FSG’s arrival, but the splurge since January 2011 has really only been an attempt to compensate for the lack of spending in previous years. This is a difficult problem to quickly address when you only have two transfer windows a year, a new phenomenon for the owners that has been difficult to adapt to, as Werner admitted, “We’re used to American sports, where there’s a draft and trades and some free agency. This is a whole different way of thinking about players.”

In any case, the net spend is still relatively low, as much of the expenditure has been recouped via player sales, especially to Chelsea who paid £50 million for Fernando Torres and £12 million for Raul Meireles. Over the last four years, Liverpool’s net spend of £22 million is much of a muchness with Manchester United and Tottenham, but a long way below the two clubs funded by wealthy benefactors, Manchester City (around £400 million) and Chelsea (over £150 million).

However, much of the damage at Liverpool is self-inflicted, as the fall-out from the Hicks and Gillett era proved very costly to the club’s finances, adding up to around £300 million, which would have bought a lot of good players or even gone a long way towards a new stadium.

This has been the toughest problem facing FSG, as they inherited a club in disarray. The situation was in some ways reminiscent of the old joke whereby a tourist asks for directions and an Irishman replies, “If I were you, I wouldn't start from here.”

Specific areas that have hurt Liverpool include: (a) hefty interest payments; (b) money lost through not qualifying for the Champions League; (c) shortfall from lower Premier League finishes; (d) compensation paid to sacked managers and executives; (e) stadium expenses written-off.

(a) In 2006, the year before Hicks and Gillett bought the club, Liverpool’s net interest payable was less than £2 million, but this rose significantly in subsequent years, peaking at £45 million in 2010 in the holding company. The total interest needlessly incurred to pay the speculators from across the pond thus amounted to a depressing £124 million.

(b) Liverpool’s failure to qualify for the Champions League last season and missing out on Europe completely this season are down to many factors, but arguably the most important was the lack of investment by the previous board, which did not provide Rafa Benitez with the means to build upon his team’s Premier League runners-up spot in 2008/09.

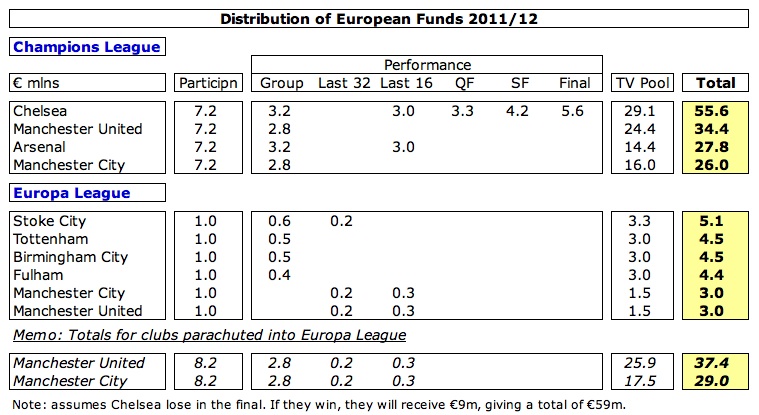

Whatever the reasons, the Reds have missed out on significant sums. Their adventures in last season’s Europa League only generated £5 million, which was significantly lower than the money received by England’s four Champions League representatives: Manchester United £44 million, Chelsea £37 million, Tottenham £26 million and Arsenal £25 million (average £33 million).

Liverpool will obviously receive nothing this season from Europe, compared to an average of £31 million for the English sides – lower than last year, as most did not progress as far. A similar sum will go begging after missing out on qualification for next season’s Champions League, giving a total of £86 million in lost revenue.

(c) Although finishing lower in the Premier League will have hurt Liverpool’s pride, it has not damaged the bank balance too much, thanks to the equitable nature of the distribution of central funds. Half of the domestic money and all of the overseas rights are split evenly among the 20 clubs, meaning that Liverpool have only really been hit by lower merit payments with each place in the league worth around £0.8 million. The other variable is facility fees, based on how often a club is shown live on television, but Liverpool’s box office appeal has ensured that this remains high.

So, Liverpool’s positions of seventh in 2009/10, sixth in 2010/11 and eighth (currently) in 2011/12 only have a minor financial effect, which we can calculate as £7 million (compared to finishing in the top four).

(d) Liverpool have paid out £20 million in compensation to sacked employees in the last three years: 2009 £4.3 million to Rick Parry, the former chief executive, and coaching staff at the Academy; 2010 £7.8 million to Benitez and his backroom staff: 2011 £8.4m to Hodgson’s team plus Purslow.

(e) The £50 million write-off for the Stanley Park scheme this year should come as no surprise, as the 2009/10 accounts had warned, “It is highly likely there will be a significant write-off of the new stadium project costs in the financial year ending 31 July 2011.” These are costs that had previously been capitalised on the balance sheet, but are now booked to the profit and loss account. Added to £10 million of similar impairment costs in 2007, that makes an incredible £60 million squandered on useless stadium designs.

"My name is Lucas"

Some of the assumptions used in this analysis may be debatable, but there is no dispute that Liverpool have thrown away a vast amount of money – more than a quarter of a billion pounds per my calculations. As the late, great Ian Dury said, “What a waste.”

Enough of past sins, let’s look at the major challenges facing Liverpool:

1. New/redeveloped Stadium

Ayre has admitted that the lack of a solution to the stadium issue has set the club back several years, “If we had started building a stadium in 2007, we would be in it by now.”

Although Anfield is a wonderfully atmospheric old ground, its relatively low capacity of just over 45,000 means that Liverpool’s match day revenue of £41 million, while more than most teams, is £68 million below Manchester United’s £109 million and less than half of Arsenal’s £93 million. Liverpool only earn around £1.5 million from each home match, which is significantly less than United (£3.7 million) and Arsenal (£3.3 million), despite significant price increases in each of the last two seasons and having the fifth highest Premier League attendance.

FSG continue to review possibilities with recent reports suggesting that the preferred option is a return to 2003 plans for a 60,000-seat stadium in Stanley Park, which were long ago given planning permission by the local council. However, the feeling persists that they would rather redevelop Anfield in the same way that they refurbished Fenway Park, the iconic home of the Boston Red Sox, as Henry confirmed, “Anfield would certainly be our first choice. But realities may dictate otherwise. So many obstacles.”

This is partly for sentimental reasons, but also for hard commercial motives, which Henry explained, “If a new stadium is constructed with 60,000 seats, you’ve spent an incredible sum of money to add just 15,000 seats. If the cost is £300 million, that doesn’t make any sense at all. Liverpool isn’t London, you can’t charge £1 million for a long-term club seat. And concession revenues per seat aren’t that much different at Emirates from Anfield.”

He added that this is why the club is seeking a naming rights partner. While Werner has categorically stated that they “have no intention of exploring naming rights for Anfield”, there would be no hesitation in following Arsenal’s Emirates model for a new stadium. Ayre again: “The new stadium in the park comes down to economics. How do we pay it back? It needs a big naming partner.”

This is easier said than done, as many clubs have discovered, but it could be a compelling prospect for sponsors, so a £150 million multi-year agreement is feasible. This would finance half of the stadium costs, leaving £150 million to be covered by additional debt, as it is unlikely to be funded by the FSG partners. Again, this could follow the Arsenal path of low interest bonds. Even in the current tough economic climate, this is where FSG’s connections should help.

"Move like Agger"

Henry stated that “from a financial perspective… a ground share (with Everton) would be helpful”, but he accepted that the lack of support from both sets of supporters means that this is effectively a dead issue.

Notwithstanding all the difficulties, the absence of a clear stadium strategy after 18 months in charge must be disappointing to Liverpool fans. Most worryingly, an email from Ayre that Tom Hicks produced in court evidence implies that Henry’s purchase agreement included “no actual guarantee of a stadium”, which is bizarre, as this was described as the only non-negotiable element by Martin Broughton, the man brought into Liverpool as chairman to sell the club. Given the broken promises in the past, it is better that the new owners take their time and get it right, but it’s not as if they have too many options.

2. Champions League qualification

Although Ayre has said that the club’s business model does not “fall apart when we don’t have a year playing European football”, it’s still a lot of money to leave on the table, e.g. in 2009/10, the last year Liverpool qualified for the Champions League, they earned £29 million.

This year, of course, they will get nothing from Europe, compared to at least £46 million that Chelsea will receive for reaching the Champions League final, which only emphasises the potential size of the prize. Additional gate receipts and higher payments from success clauses in commercial deals also contribute to what Ayre calls a “significant revenue uplift”.

Gate receipts are important, as Liverpool’s last two seasons both included income from seven additional matches, which was worth around £10 million. This will not be the case in 2011/12 with no European competition, though domestic cup runs will partially offset the shortfall. However, the Europa League will contribute again next season (albeit probably lower attendances at reduced prices).

It is also imperative that Liverpool reclaim their traditional place among Europe’s elite (remember that they have won this prestigious competition no fewer than five times) in order to help attract world-class players to Anfield.

3. Revenue growth

FSG will be looking at revenue growth in terms of both short-term gains and longer-term possibilities.

More immediately, the focus is on commercial income, which rose an impressive 25% last season to £77 million. This is already the seventh highest in Europe, though it is a fair way behind Manchester United £103 million and only around half the amount earned by Bayern Munich, Real Madrid and Barcelona. As Ayre said, “We’ve made great progress but… we still have a long way to go particularly internationally.”

Most of the growth came from the four-year shirt sponsorship deal with Standard Chartered, which is worth around £20 million a year, so £12.5 million higher than the previous deal with Carlsberg. This is in line with Manchester United’s Aon deal and Manchester City’s reported Etihad agreement, but Barcelona’s £25 million contract with the Qatar Foundation has raised the bar.

Future growth is assured by the £25 million kit deal with Warrior Sports, which is not included in the latest results. Starting from the 2012/13 season, this is more than twice the amount received from Adidas, who currently pay £12 million a year, and is about the same level as Manchester United, Real Madrid and Barcelona. This makes sense, as these are the leading clubs in terms of replica shirt sales worldwide.

Interestingly, unlike the Adidas arrangement, Liverpool will be allowed to open their own retail outlets, which some have speculated might mean doubling the value of the deal to £300 million over six years, as Ayre noted, “That area of business currently represents 50% of everything we generate.” Of course, that is revenue, which is not the same as profit, and it is a policy that Manchester United abandoned in the 1990s when they joined forces with Nike, so it might not be the El Dorado many assume.

In addition, the club will surely look to emulate United’s success in attracting secondary sponsors, which will be helped by FSG’s ability to package the Liverpool brand with their other sports holdings to provide an attractive opportunity to advertisers, as they did with Warrior. As Ayre put it, “The more quality and high-level partners we can attract, the more we’ll have to invest.”

There are numerous possibilities to “leverage the club’s global following to deliver revenue growth”, which was emphasised by Werner, “We consider Liverpool to have untapped potential globally.” In particular, they have focused on Asia with plans to open two new offices there, supported by a pre-season tour that attracted huge crowds – a key element in securing the Standard Chartered sponsorship. They will build on this success by again touring the Far East plus the US, including a match at Fenway Park against Roma.

"Suarez - I fought the law"

One unexpected threat to this campaign emerged earlier this season when Standard Chartered expressed their unhappiness with the bad publicity around the Suarez affair, but a bigger danger would be a continued lack of sporting success. As Ayre said, “performance on the pitch definitely affects business.”

In the longer-term, FSG will be pushing to further “monetise” Liverpool’s global appeal, especially in the television space. They were attracted by the explosive growth in overseas TV rights for the Premier League, backed up by top matches attracting huge global audiences.

This is particularly relevant to Liverpool, as FSG have substantial expertise in this sphere, owning 80% of New England Sports Network, a profitable regional cable television network, while Werner is an experienced television producer. This may have been behind Ayre’s unpopular suggestion that leading clubs should receive a larger slice of the money from overseas TV rights, because the average fan in Kuala Lumpur “isn’t subscribing… to watch Bolton.”

New technology will open up a plethora of possibilities for digital rights, which to date have been treated as little more than an afterthought to the main TV deal, but the emergence of fast, broadband networks might just be the catalyst for clubs to interact directly with fans, when revenue could potentially explode. If so, you can expect Liverpool to be at the forefront of any such developments.

"Jordan: the comeback"

4. UEFA’s Financial Fair Play regulations

Another motive for the club to increase revenue is the advent of UEFA’s Financial Fair Play (FFP) rules that aim to make clubs live within their means, rather than operate with big losses bank-rolled by wealthy benefactors.

The first monitoring period is 2013/14, but this will take into account losses made in the two preceding years, namely 2011/12 and 2012/13. In other words, the 2010/11 accounts are not considered, but those from the current season will be, so a rapid improvement is required.

However, they don’t need to be absolutely perfect, as owners will be allowed to absorb aggregate losses of €45 million (around £38 million), initially over two years and then over three years, as long as they cover the deficit by making equity contributions.

Not only is Henry supportive of these regulations, but he said “we wouldn’t have moved forward on Liverpool except for the passage of FFP.” However, he is concerned that others will find ways around the rules, “The question remains as to how serious UEFA is regarding this. It appears that there are a couple of large English clubs that are sending a strong message that they aren’t taking them seriously.” He specifically queried the transparency of Manchester City’s massive Etihad deal, given the owners’ close relationship with the sponsors. Werner supported the party line, hoping that UEFA’s process “would have some teeth.”

One point to note is that the cost of a new stadium would be excluded from UEFA’s break-even calculation, so that should not be a factor in any investment decision.

5. Cut costs

Given the revenue pressures arising from the lack of Champions League, Liverpool will have to cut their cloth accordingly, which means reducing the wage bill. After purchasing the club, Henry complained about “a huge multi-year payroll for a squad that had little depth.”

Action was taken last summer with many bit part players leaving either through sales (including Meireles, Paul Konchesky, Milan Jovanovic, David N’Gog, Sotirios Kyrgiakos, Emiliano Insua and Philipp Degen) or loans (notably Joe Cole and Alberto Aquilani), even if this meant cut-price deals or subsidising loans. Obviously, there have been a fair few arrivals too, so the net impact is unknown, but is likely to be positive in the next accounts.

The danger of this approach is that other clubs continue to grow their wage bill, which traditionally has a high correlation with success on the pitch. That said, Tottenham have outperformed Liverpool recently with a far lower payroll.

"Would you Adam and Eve it?"

While FSG were initially attracted to Liverpool by parallels with the Red Sox, another great club that had fallen on hard times and needed a stadium solution, there were also sound business reasons behind the investment, even though Henry has stated, “I don’t think you go into sport to make a profit.” In particular, if they succeed in driving revenue growth, they will be able to keep all the money they make (apart from some of the TV rights), unlike baseball where their income is taxed by the MLB and shared among other clubs.

Despite the obvious synergies, both clubs have suffered recently in the sporting arena, Liverpool enduring their worst run of results in the league for over 50 years, while the Red Sox spectacularly collapsed to miss out on qualification for the post-season play-offs. This has raised concerns that FSG are being spread too thin, though their template leans heavily on the managers of the franchise, mainly Ayre, Dalglish and (until recently) Damien Comolli, the Director of Football.

In fact, FSG’s mantra has long been one of self-sufficiency for Liverpool. This will be a challenge, as their cash flow has been consistently negative before financing – except when investment in the squad and stadium is restricted like in 2010. The problem is that this is exactly what Liverpool need, hence the dash for cash with new sponsorship deals.

A key element of FSG’s strategy is a focus on youth, as outlined by Henry, “We have been successful through spending and through securing and developing young players.” Werner added, “We certainly feel we can do a better job bringing in more players that are home grown.”

Dalglish has been more than willing to follow this policy, acknowledging the improvements, “You look at the academy and see how much better it is.” Many graduates have been given first team action this season (Jay Spearing, Martin Kelly, John Flanagan and Raheem Sterling), which is testament to the changes implemented by Benitez, as is the high number of Liverpool youngsters involved in England squads.

When FSG first appeared on the scene, much was made of their belief in the application of statistical analysis made famous by Moneyball, Michael Lewis’ bestseller about the innovative methods adopted by Billy Beane at the Oakland Athletics baseball club. However, it was never quite that simple, as Henry acknowledged, “Everyone is fixated on Moneyball or sabermetrics, but football is too dynamic to focus on that. Ultimately you have to rely on your scouting.”

"Carroll - big deal"

It has always been the case that they have used their financial muscle to complement value purchases by also spending big on players that they needed. In fact, the Red Sox have been among the highest spenders in major league baseball. That said, some of the prices paid for Liverpool’s purchases have looked ridiculous, especially considering the good use that Newcastle have made with the money Liverpool paid them for Carroll. Ultimately, that was one of the reasons for Comolli being given his P45. As Werner wryly explained, “We’ve had a strategy that we agreed on. There was some disconnect on the implementation of that.”

The investment in the academy and scouting is all very worthy, but in the meantime the first team has been under-performing, so it is legitimate to ask whether FSG’s strategy is the right one for Liverpool. After all, when Henry bought the club, he confessed to knowing “virtually nothing about Liverpool Football Club nor EPL.” A year later, he said, “We have so much to learn about all aspects of the sport and we are still learning.”

Some fans are crying out for stronger leadership, which often translates into additional investment, both in the playing squad and the stadium. Conversely, FSG might argue that they could have expected a better return on the money they have put in (even though the acquisition was concluded at a “fire sale” price of £300 million). Ayre is firmly supportive, “Money is not an issue. If we need somebody, I think our owners have shown the level of commitment you would expect from a good ownership group.” Mind you, he said that before the late season slump.

"The Kuyt Runner"

It was always a big ask to secure Champions League qualification in the first full season under new ownership, but there’s little doubt that Liverpool’s results have been below par. Although by no means disastrous, it has been a disappointing season, leading to Dalglish’s position being questioned.

Henry has shown that he is not afraid of pulling the trigger, especially when the long-serving Red Sox manager Terry Francona was effectively fired last summer. The removal of Comolli confirmed that FSG could be just as ruthless at Liverpool, with Werner observing, “when it’s time to act, we need to act”, but Henry recognises that the rebuilding process at Anfield will take time, “it could take years to get the club back to where it needs to be.”

Even though the team might be lagging behind expectations, there has been some improvement under FSG, which was recognised by stalwart Jamie Carragher, “people need to remember the club was on its knees.” Years of mismanagement has cost Liverpool hundreds of millions, but Ayre for one is now positive, “The key message is that the new ownership has created stability, a long-term opportunity for Liverpool and some good foundation work that hopefully we’ll all build on.”

"Hope in the Ayre"

Nevertheless, the fans will want to see more progress where it counts, as Ayre acknowledged, “The finances are all well and good – if you don’t have any finances, it makes it more difficult to be successful – but success on the pitch is the biggest factor.”

There may well be changes on the playing side (and even in the manager’s seat) this summer, but to date FSG have backed their man, taking a patient, level-headed view of the club’s prospects, as seen by Werner’s pre-season objective, “We just want to move forward – we want to be better this year than last year and just keep going on the right track.” In other words, keep calm and carry on.

0 comments:

Post a Comment