In the past few years there has been tremendous progress in football fans’ knowledge of their clubs’ finances. Some might say that this is not a good thing and we should focus on matters on the pitch. That’s perfectly fair, indeed I would also personally much prefer to watch a great game, such as Borussia Dortmund’s recent demolition of Real Madrid, rather than investigate the minutiae of their balance sheets.

However, it is important that fans are aware of what is going on at their club, so that they understand the board’s strategy and any constraints that impact their activities, e.g. why a club might sell its best players every summer or why a club does not splash out on the world-class striker that might take them to the next level.

Traditionally, supporters have concentrated on a club’s profit and loss account, which is not surprising, because: (a) that is what the media tends to report – on the back of press releases from the clubs; (b) it is intuitively easy to understand, being essentially revenue less expenses (mainly player wages).

Nevertheless, the reported figure is an accounting profit, which is not necessarily a “real” profit, as it is based on the accountant’s accruals concept and this can be very different from actual cash movements. This was noted recently by, of all people, Simon Jordan, the former Crystal Palace chairman, on Sky’s excellent Footballers’ Football Show, as he claimed that the reported profit at football clubs was depressed by non-cash items.

"Jordan: The Comeback"

The perma-tanned, Spandau Ballet look-alike, actually has a point. As the old saying goes, turnover is vanity, profit is sanity, but cash is king. The main reason that football clubs like Portsmouth fail is cash flow problems. It does not matter how large your revenue is (or your profits are), if you do not have the cash to pay your players, suppliers or the taxman, then you are going to crash into the rocks.

Therefore, this blog is going to focus on the cash flow at each of the Premier League clubs in 2011/12 (the last season where all clubs have published detailed accounts). It will start with the familiar profit and loss account, highlighting the accounting shenanigans, and then reconcile this with the cash flow statement.

We shall then examine how football clubs really spend their money, revealing the different business models that are employed and explaining why certain clubs act as they do, including a review of the top seven clubs in the league (Manchester United, Manchester City, Chelsea, Arsenal, Tottenham, Everton and Liverpool).

Profit and Loss Account

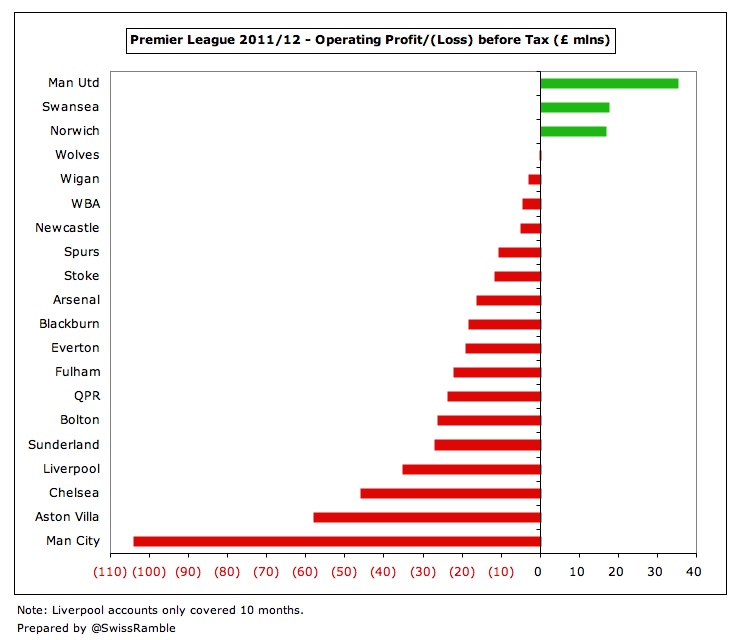

The total turnover in the 2011/12 Premier League amounted to a hefty £2.3 billion, but still only produced an operating loss of £363 million, mainly due to wages of £1.6 billion, giving a wages to turnover ratio of 69%. There were also other expenses of £535 million and player amortisation, player impairment and depreciation of £544 million.

Only three Premier League clubs made operating profits last season: Manchester United £35 million, Swansea City £18 million and Norwich City £17 million. At the other end of the spectrum, Manchester City reported a massive operating loss of £104 million, followed by Aston Villa £58 million and Chelsea £46 million.

Clubs’ figures were boosted by £224 million profits on player sales (with the largest being Arsenal’s £65 million), though there is also £78 million net interest payable (most notably Manchester United’s £50 million), leading to £197 million loss before tax (and £179 million loss after tax).

Cash Flow from Operating Activities

The starting point for a football club’s cash flow statement is the operating profit (or more likely loss), which is converted into cash flow from operating activities via two adjustments: (a) adding back non-cash items such as player amortisation, depreciation and player impairment; (b) movements in working capital.

(a) Non-cash Items

First of all, we need to understand how football clubs account for transfer fees. Instead of expensing these completely in the year of purchase, players are treated as assets, whereby their value is written-off evenly over the length of their contract via player amortisation. As an example, Manchester United signed Robin van Persie for £22m on a four-year contract, so the annual amortisation is £5.5 million (£22 million divided by four years).

Similarly, tangible fixed assets like a club’s stadium and training ground are also depreciated, though their useful life is considerably longer. Player impairment occurs when the club decides that the value of a player in its accounts is too high, e.g. the player suffers a career threatening injury, loss of form or is in dispute with the management.

Incidentally, this also highlights why profit on a player sales is not a real cash figure, as this represents sales proceeds less the carrying value in the books. So, if van Persie were to be sold after three years for £7 million (i.e. £15 million lower than his £22m cost), there would still be a reported profit of £1.5 million, as his value in the accounts would be only £5.5 million (£22 million cost less three years amortisation at £5.5 million a year).

(b) Movements in Working Capital

Working capital is a measure of a club’s short-term liquidity and is defined as current assets less current liabilities. Changes in working capital can cause net income (in the profit and loss account) to differ from operating cash flow. Clubs book revenue and expenses when they occur instead of when the cash actually changes hands, e.g. if the club buys equipment from a supplier it would record the expense even before it pays the cash.

If current liabilities increase during the year, the club is able to pay its suppliers more slowly, so the club is (effectively) temporarily holding onto cash, which is positive for cash flow. On the other hand, if a club’s debtors increase, this means that it collected less money from its customers than it recorded as revenue, so that would be negative for cash flow.

In most years, the working capital movements will not be that significant, though it can be a high figure, e.g. £43 million at Manchester City and £39 million at Chelsea.

Adding back £544 million non-cash items and £(95) million working capital movements to the reported operating loss of £363 million does indeed make a big difference, as the cash flow from operating activities becomes a positive £87 million.

In fact, 12 of the Premier League clubs have positive operating cash flow (up from 3 with operating profits) with Manchester United leading the way with an impressive £80 million, followed by Norwich City £30 million, Arsenal £28 million and Tottenham £27 million. Even Manchester City’s negative operating cash flow of £53 million is only about half of their £104 million operating loss, mainly because their P&L includes an enormous £83 million player amortisation, arising from their big spending in the transfer market.

Cash Flow before Financing

The operating cash flow is in theory what is then available to the club to spend on buying players, investing in infrastructure or paying interest on loans and (occasionally) tax, though additional financing may be secured to cover any shortfalls.

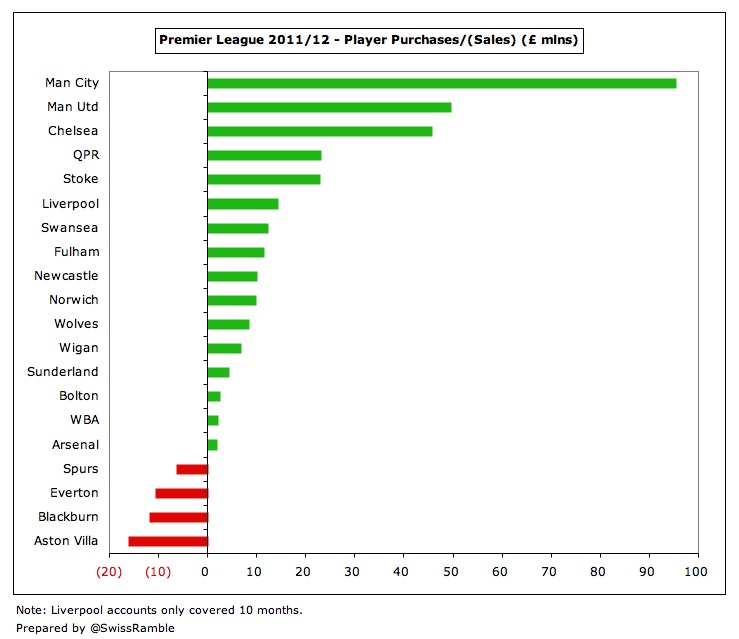

(a) Net Player Purchases

This represents the genuine cash payments for player purchases less any sales and is often very different from the net spend reported in the media, largely because of stage payments, though it can also be affected by agents’ fees and conditional payments, e.g. based on number of appearances or trophies won. It is the only authentic figure publicly available for transfer fees, but it can also be misleading, as it may not cover the entire fee due to stage payments.

Paying transfer fees in stages can be a significant source of financing for some clubs, e.g. Juventus owed €93 million to other clubs (“for the acquisition of players”) as of June 2012, though they were in turn owed €41 million by other clubs.

On a cash basis, the highest net player purchases in the 2011/12 Premier League unsurprisingly came from Manchester City with £95 million (£123 million purchases less £28 million sales), followed by Manchester United £50 million, Chelsea £46 million and (shock, horror) struggling QPR and Stoke City, both with £23 million.

Four clubs actually made net player sales, i.e. used the transfer market as an additional source of funds: Aston Villa £16 million, Blackburn Rovers £12 million, Everton £11 million and Tottenham £6 million.

Arsenal just about balanced their books with £57 million purchases and £56 million of sales, giving net player purchases of £2 million. It is worth noting that this is considerably lower than the £65 million profit on player sales reported in the accounts.

(b) Investment in Fixed Assets

Clubs invested £142 million in fixed assets in 2011/12, mainly for development of the stadium and training centre, with 77% coming from just four clubs: Tottenham £42 million, Manchester City £30 million, Manchester United £23 million and Wolves £15 million.

(b) Net Interest Paid

This is very largely interest paid on bank loans net of any interest received from cash balances. One figure stands out here and that is the £46 million paid by Manchester United, which is over three times as much as the nearest “challenger”, namely Arsenal with £13 million. Given that United still had £437 million of gross debt at the time of the 2012 accounts, way more than any other club in the Premier League, this is not too unexpected. It has also not proved to be a major obstacle to United’s financial stability, as their cash flow is more than sufficient to cover the annual interest payments.

We should also note here that interest paid is not necessarily equal to the interest payable figure in the profit and loss account, as interest is sometimes accrued (so not paid), thus increasing the size of the debt, e.g. this is the case with a number of Championship clubs, including Cardiff City, Leicester City and Ipswich Town.

(c) Tax

Even though nine Premier League clubs reported profits before tax in 2011/12, only four (Arsenal, Manchester United, West Bromwich Albion and Tottenham) actually paid any tax. This is a very complex subject, but, essentially, use of prior year losses and other allowances helped prevent tax payments.

After all this expenditure, we have cash flow before financing, which is perhaps the purest reflection of how a club has run its business. By this metric, the newly promoted Norwich City and Swansea City shine with positive cash flow of £18 million and £6 million respectively. Most clubs clearly strive to break-even with many hovering around zero net cash flow.

Interestingly, and maybe disappointingly, the three clubs with the largest negative cash flows feature strongly at the top of the league: Manchester City £(184) million, Chelsea £(72) million and champions elect Manchester United £(41) million.

Financing

However, that is before financing and this is where the owners play their part, either via issuing share capital (Manchester City £169 million) or making additional loans (Chelsea £71 million, subsequently converted to capital). Other clubs required funds from their benefactors, notably QPR £39 million, Bolton Wanderers £24 million, Liverpool £24 million and Blackburn Rovers £16 million.

On the other hand, some clubs actually used funds to reduce debt, including Wigan £39 million (converted to share capital), Manchester United £29 million, Newcastle United £11 million, Arsenal £6 million and Norwich City £5 million.

Cash Flow after Financing

After this financing, we can see that almost all clubs are within the range of £18 million positive cash flow and a manageable £18 million negative cash flow. The one exception is Manchester United, which is a special case as a result of the Glazers’ leveraged buy-out. In 2011/12 alone, United paid £85 million to support this transaction: £46 million interest, £29 million loan repayments and £10 million dividends to the owners.

Let’s look at how cash flow has impacted the actions of the seven leading clubs in the Premier League.

Arsenal

Long admired for their financial prowess, Arsenal have consistently reported large profits. Not only did they register the highest profit before tax (£37 million) in the Premier League in 2011/12 on the back of £235 million turnover (3rd highest in England, 6th highest in the world), but they have also made an incredible £190 million of profits in the last five years. Indeed, the last year that they made a loss was a decade ago in 2002.

However, much of this excellent performance has been down to profits from player sales (e.g. £65 million in 2011/12) and property development (e.g. £13 million in 2010/11), while the operating profit has been steadily declining with the club actually reporting an operating loss of £16 million last season.

That said, once sizeable non-cash expenses (amortisation and depreciation) and working capital movements are added back, the cash flow from operating activities was £28 million, which was actually the third best in the Premier League.

The problem is that Arsenal have spent very little of this on improving their squad: in 2011/12 the net expenditure on player purchases was just £1.8 million – only four clubs spent less than the Gunners. Most of the available funds have instead gone towards financing the Emirates Stadium: £13.1 interest and £6.2 million on debt repayments. A further £8.6 million was invested in fixed assets for enhancements to Club Level, more “Arsenalisation” of the stadium and new medical facilities and pitches at the London Colney training ground.

Arsenal have cleared all their property development debt, but still had £253 million of gross debt arising from long-term bonds that represent the “mortgage” on the stadium (£225 million) and the debentures held by supporters (£27 million). Once cash balances of £154 million were deducted, net debt was only £99 million, but the interest/debt payment schedule remains punishing.

Despite the high interest charges, it is unlikely that Arsenal will pay off the outstanding debt early. The bonds mature between 2029 and 2031, but if the club were to repay them early, they would then have to pay off the present value of all the future cash flows, which is greater than the outstanding debt.

Another logical result of Arsenal’s years of reported profits is that they are one of the few Premier League clubs that pay corporation tax: £4.6 million last season (the highest in the league).

"Mind over Money"

So Arsenal’s self-sustaining approach is clearly evident in the cash flow statement, though they did have a small negative cash flow after financing in 2011/12 of £6.6 million. The supporters would almost certainly prefer to see the club spending more on players, rather than areas off the pitch, but the reality is that the debt and interest payments are not going away anytime soon.

This was made very clear by Arsène Wenger, “We want to pay the debt back from building the stadium and that’s around £15 million, so it’s normal that at the start we have to make £15 million or we lose money.” In fact, as we have seen, it’s more like £19 million, but the point remains valid.

However, the lack of investment in the squad is still galling, especially with Arsenal’s cash balances standing at £154 million last summer (almost as much as the rest of the Premier League clubs put together) following many years of positive cash flow, e.g. 2010/11 £33 million, 2009/10 £28 million, 2008/09 £6 million, 2007/08 £19 million and 2006/07 £38 million.

In the future, cash should be boosted by commercial income rising with the recent Emirates shirt sponsorship agreement and a new kit supplier deal, but Champions League qualification will also be important.

Manchester City

Despite rapidly growing their revenue to £231 million (4th highest in England), City still reported a pre-tax loss of £99 million, largely because of a £202 million wage bill, though in fairness this was nearly £100 million better than the previous year’s £197 million loss. The improvement is due to success on the pitch (2011/12 Premier League winners and Champions League qualification) and new sponsorship agreements, especially the Etihad deal.

City can add back £90 million for non-cash expenses, mainly £83 million player amortisation, but they also have £39 million negative working capital adjustments, due to an increase in debtors, leading to £53 million negative operating cash flow (the worst in the league).

Nevertheless, City spent much more than anybody else on player purchases (net £95 million) and £30 million on fixed assets, mainly on the Etihad Campus, including the City Football Academy, plus some stadium refurbishment.

"The minute you walked in the joint..."

They also have to pay £6 million interest, despite no debt from the owners Abu Dhabi United Group, as the club still has some old loan notes and finance leases.

That business model produces an enormous negative cash flow before financing of £184 million, which is then almost entirely covered by financing from the owner in the form of new share capital.

In the future, City should continue to grow their commercial income, while we have also seen a slowing of their player investment in the light of UEFA’s Financial Fair Play regulations.

Chelsea

Very similar to Manchester City’s strategy, but the football club actually reported a £1.4 million profit in 2011/12 after their Champions League success, though this was also due to an £18.4 million exceptional gain after the cancellation of preference shares owned by British Sky Broadcasting and £29 million profit on player sales. Net turnover rose to £256 million, but the £176 million wage bill was only surpassed by Manchester City, giving rise to an operating loss of £46 million.

Chelsea’s large non-cash expenses of £61 million are added back, but they also have £43 million negative working capital adjustments, mainly due to a large decrease in creditors, leading to £27 million negative operating cash flow.

Again, they spent heavily on players (net £50 million) and invested £5 million in fixed assets. Cash was also boosted by £6 million from the acquisition of a subsidiary, Chelsea Digital Media Limited, which was transferred from a joint venture to a 100% owned subsidiary.

"From Russia with Money"

All that produced a hefty negative cash flow before financing of £72 million, the second worst in the league, which was covered by an additional loan from the parent company, Fordstam Limited, owned by Roman Abramovich. As per previous years, this loan was subsequently converted into share capital, so the football club has no debt.

That said, it is not really true to say that Chelsea is debt-free, as these loans still exist in the holding company, amounting to £895 million as at June 2012. They are interest free, but are repayable with 18 months notice. It must be considered unlikely that Abramovich would ever call in this debt, but it is theoretically possible.

It looks like Chelsea are trying to reduce their wage bill to ensure they break-even, but their revenue will be under some pressure, as last season was boosted by the Champions League triumph, though new commercial deals were signed in 2012/13, notably Gazprom and Audi.

Liverpool

Despite their accounts only covering 10 months, due to a change in accounting date, Liverpool’s reported revenue of £169 million was still the 5th highest in England. Deloitte estimated that it would be £189 million for a full year. However, the Reds’ loss of £41 million was the second worst in the country, due to a £109 million wage bill (£131 million on an annualised basis) and £10 million of termination payments to coaching staff.

The £35 million operating loss was improved by adding back £46 million non-cash items (mainly £34 million player amortisation, but also including £9 million for player impairment), offset by £12 million working capital movements, to give negative operating cash flow of around £1 million.

Only five clubs had higher net player purchases than Liverpool’s £14 million, though this still placed them behind QPR and Stoke City, both with £23 million. This figure is a little misleading, as Liverpool spent relatively high on player purchases (£45 million), but largely compensated for this expenditure with £31 million from player sales.

"May you live in less interesting times"

Liverpool also made £3.7 million interest payments, though this was significantly lower than the sums paid during the dark days of the Hicks and Gillett era, which were as high as £45 million in 2010.

The £21 million negative cash flow before financing was fully covered by additional bank loans, leading to a small positive cash flow of £2 million.

Liverpool’s debt in the last annual accounts was £92 million, split between £70 million bank loans and £22 million to the owners Fenway Sports Group, but since then John W. Henry and his fellow investors have put in £47 million to reduce bank debt in August. These loans are interest-free, so interest payments should further reduce (at least until new loans are taken out for stadium development).

Redevelopment of Anfield should boost match day revenue in the future, though it will require substantial funding. In the meantime, Liverpool continue to sign impressive commercial deals, e.g. Chevrolet and Paddy Power, though lack of qualification for the Champions League places them at a severe financial disadvantage to other leading clubs.

Tottenham Hotspur

Tottenham made a £7.3 million loss before tax after revenue fell to £144 million (from £164 million the previous year), due to only qualifying for the Europa League instead of the more lucrative Champions League. The wage bill was held at £90 million, leading to an operating loss of £11 million.

Adding back £35 million for player amortisation and depreciation plus £3 million for working capital movements, due to a rise in creditors, means that cash flow from operating activities was a healthy £27 million.

This was boosted by net player sales of £6 million (player sales £33 million, purchases £27 million) with Spurs being one of only four Premier League clubs to generate cash from this activity.

"Stadium Arcadium"

At the moment Spurs are investing almost all their surplus cash in fixed assets, having spent £42 million last season on plans for a new stadium (Northumberland Development Project) and the new training centre in Enfield. This was more than any other Premier League club spent on infrastructure in 2011/12. In addition, they paid £4.5 million interest, as debt climbed to £86 million, made up of bank loans and securitisation funds.

After the significant investment off the pitch Tottenham’s cash flow before financing was a negative £13 million, partly financed by £8 million additional bank loans, leading to negative net cash flow of £5 million.

Tottenham’s financial future will be dictated to a very large extent by what happens with the stadium development, though they would be greatly helped if they could again qualify for the Champions League. The club estimated that the 2011/12 Europa League campaign brought in £31 million less revenue than the previous season’s foray into the Champions League.

Everton

Everton made a loss of £9 million from revenue of £81 million and a wage bill of £63 million (10th highest in the Premier League). The operating loss of £19 million was improved by adding back £14 million of player amortisation and depreciation less a working capital adjustment of £2 million, giving a negative cash flow from operating activities of £7 million.

Everton’s need to box clever is highlighted by the fact that even after net player receipts of £11 million (sales £23 million, purchases £13 million), they do not quite manage to break-even with negative cash flow after financing of £2 million. All other things being equal, they need to sell a player every season to stay afloat.

This is due to £4 million interest payments and £0.9 million repayment on assorted loans. The club’s debt stands at £49 million with an £11 million overdraft plus £24 million loan notes (borrowed against future season ticket sales) and £14 million loans (borrowed against future TV money). The lending arrangements with Barclays Bank expire on 31 July 2013, so these will have to be renegotiated in a few months.

Manchester United

Despite having the highest revenue in England (£320 million) and incidentally the 3rd highest in the world (only beaten by Real Madrid and Barcelona), United made a £5m loss before tax in 2011/12. This had very little to do with the club’s underlying business, as United’s £35 million operating profit was actually the highest in the Premier League, even after a £162 million wage bill.

No, the negative bottom line is due to £50 million net interest payable which is the consequence of the Glazer family’s leveraged takeover that placed over half a billion pounds of debt on the club’s balance sheet in 2005.

In fact, after adding back £46 million of player amortisation and depreciation less a minor working capital adjustment, United’s cash flow from operating activities is a highly impressive £80 million (in the previous year this was an almost unbelievable £125 million). To place that into context, this is £53 million more than the widely praised Arsenal. Quoting Staines’ finest, Hard-Fi, United are a veritable “cash machine”.

Over the last few years, relatively little of this wealth has been spent on improving the squad. Indeed, between 2009 and 2011, United actually had net sales proceeds of £3 million – though this was admittedly greatly helped by Ronaldo’s £80 million sale to Real Madrid. However, in 2011/12 the Glazers turned on the taps with United allocating £50 million to net player purchases, only surpassed by their neighbours Manchester City.

They also invested £23 million in fixed assets, mainly land and buildings around Old Trafford.

However, what really stands out is the £46 million interest United had to pay. This is by far the highest in the Premier League with Arsenal the only other club having to make a double-digit interest payment (£13 million). In fact, United pay about the same amount of interest as all the other Premier League clubs combined.

"Brass in Pocket"

A £3 million tax payment resulted in £41 million negative cash flow before financing, while £29 million loan repayments and £10 million dividends to the Glazers (to repay loans borrowed from the club in 2010) meant £80 million negative cash flow after financing – the worst in the Premier League.

It really is a game of two halves at United with £80 million of operating cash flow converted into negative cash flow after financing of £80 million. That £160 million swing can be broadly split between £72 million healthy spend (player purchases £50 million and property investment £23 million) and £88 million unwanted spend (interest £46 million, debt repayment £29 million, dividend £10 million and tax £3 million).

Although debt has been significantly reduced from the horrific £773 million peak in 2010, it still stood at £437 million (net £366 million after deducting £71 million cash) as at 30 June 2012, mainly senior secured notes attracting interest rates between 8.375% and 8.75%.

Looked at another way, without the burden of the Glazers’ debt, United could afford to spend £80 million every season on new players. And that is before the amazing new commercial deals with Chevrolet (shirt sponsorship) and Aon (training ground naming rights) kick in, not forgetting the likelihood of a major uplift when the kit supplier deal is re-negotiated (Nike runs to July 2015).

"Come on, Alex. You can do it."

Obviously, United have not done too badly in recent years, but they might well have done even better with those additional funds being made available to the manager, especially in Europe, where they have struggled for the last two seasons. Arguably, that’s the best argument in favour of the Glazers, namely that they have made it easier for other clubs to compete. Without their grasping presence, United would, quite literally, be laughing all the way to the bank.

That said, there are signs that this financial burden may be easing, as half of the proceeds from last August’s IPO were used to reduce debt to £367 million by December 2012, so annual interest paid should fall, though it is difficult to estimate a precise figure, given the many factors involved, such as exchange rates on the USD element of the debt.

If the club uses the additional revenue from its own commercial growth and the new Premier League TV deal (worth at least another £30 million a season) for more debt reduction, then the interest payments will become less significant, freeing up even more cash – though that might just be used to pay the Glazers dividends…

"Running up that Hill (A Deal with God)"

Of course, the new Premier League TV deal that commences next season will benefit all clubs in the top flight and should make a real difference to their ability to generate cash, especially in conjunction with the new Premier League Financial Fair Play (FFP) regulations. These state that clubs are only allowed to make a total loss of £105 million providing this is covered by the owner (and £90 million of that is injected into the club in the form of equity).

Furthermore, clubs with wage bills above £52 million will only be allowed to increase their wages by £4 million per season for the next three years, though that restriction only applies to TV money, so clubs are free to spend any additional income from ticket sales or commercial deals on wage growth.

One of the objectives behind these regulations is that, in contrast to previous deals, the increase in TV money will not simply disappear into the players’ wage packets. This could markedly improve clubs’ cash flow, though there is a chance that any surplus may be simply used to pay dividends to the owners, as opposed to, say, reducing ticket prices, investing in youth development or improving facilities for the fans.

"A Change is Gonna Come"

Similarly, UEFA’s FFP regulations will encourage clubs to live within their means and are even more stringent. Wealthy owners will only be allowed to absorb aggregate losses of €45 million (£38 million), initially over two years and then over a three-year monitoring period, as long as they are willing to cover the deficit by making equity contributions. The maximum permitted loss then falls to €30 million (£25 million) from 2015/16 and will be further reduced from 2018/19 (to an unspecified amount).

To coin a phrase, this will be a whole new ball game for football clubs’ business models with the financing of large deficits by wealthy benefactors expected to significantly reduce. Whatever happens, those wishing to understand a football club’s finances and consequently the impact these have on its strategy should, as always, follow the money. That means not just focusing on the profit and loss account, but also dipping a toe into the mysterious world of the cash flow statement.

0 comments:

Post a Comment