In a series of posts over the course of the last year, I argued that you can value users and subscribers at businesses, using first principles in valuation, and have used the approach to value Uber riders, Amazon Prime members and Spotify & Netflix subscribers. With each iteration, I have learned a few things about user value and ways of distinguishing between user bases that can create substantial value from user bases that not only are incapable of creating value but can actively destroy it. I was reminded of these principles this week, first as I wrote about Walmart's $16 billion bid for 77% of Flipkart, a deal at least partially motivated by shopper numbers, then again as I read a news story about MoviePass and the potential demise of its "too good to be true" model, and finally as I tripped over a LimeBike on my walk home.

User Based Value

My attempt to build a user-based valuation model was triggered by a comment that I got on a valuation that I had done of Uber about a year ago on my blog. In that post, I approached Uber, as I would any other business, and valued it, based upon aggregated revenues, earnings and cash flows, discounted back at a company-wide cost of capital. I was taken to task for applying an old-economy valuation approach to a new-economy company and was told that that the companies of today derive their value from customers, users and subscribers. While my initial response was that you cannot pay dividends with users, I realized that there was a core truth to the critique and that companies are increasingly building their businesses around their members.

Consequently, I went back to valuation first principles, where the value of any asset is a function of its cashflows, growth and risks, and adapted that approach to valuing a user or subscriber:

To get from the value of existing users to the value of an entire company, I incorporated the value effect of new users, bringing in the cost of acquiring a new user into the value:

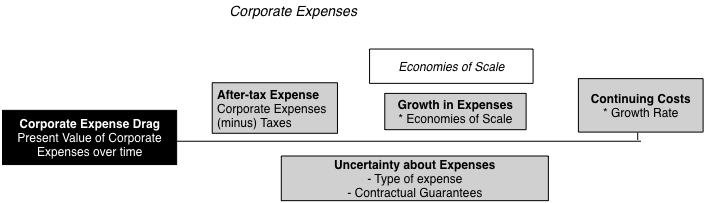

I applied closure by consider all corporate costs that are not directly related to users or subscribers in a corporate cost drag, a drag because it reduces the value of the business:

Cumulating the value of existing and new users, and netting out the corporate cost drag yields the value of operating assets, i.e., the same value that you would derive by discounting the free cash flows to the entire business by its overall cost of capital. You would still need to clean up, by adding in cash, netting out debt and dealing with outstanding options, but that process is the same in both models.

I would hasten to add that a user-based value model is not a panacea to any of the valuation challenges that we face with young, user-based companies. In fact, the difficulties with obtaining the raw data needed on user renewal rates and acquisition costs can be so daunting that any potential advantages that you obtain by looking at user-level value can be drowned out by noise. It is also worth emphasizing that its user-focus notwithstanding, this model is grounded in fundamentals, with value coming, as it always does, from cash flows, growth and risk. I am still learning about this model, but I have put down what I have learned over the last year, when valuing Uber, Amazon Prime and Netflix, into a paper that you can download, read and critique.

Good, Bad and Indifferent User-based Models

One of the motivations for my user-focused valuation was based upon casual empiricism. In my view, many venture capitalists and public investors are pricing user-based companies on user count, with only a few seriously trying to distinguish between good, indifferent and bad user-based models. One of the bonuses of using a user-based model is that it provides a framework for differentiating between great and mediocre user-based companies.

Drivers of Value

A standard critique that old-time value investors have of user-based companies is that they all lose money, but that is not true. There are user-based companies that make money, but it is also true that the user-based model is still in its infancy and that many user-based companies are young, and therefore lose money. That said, there are elements of the cost structure that you can look at, to make judgments on which user-based companies are most likely to grow out of their problems and which ones are just going to grow their problems.

a. Cost Structure: Most young, user-based companies lose money but at the risk of sounding unbalanced, there are good ways to lose money and bad ones, from a value perspective.

- Servicing Existing Users versus New User Acquisition: From a value perspective, it is far better for a company to be losing money, because it is spending money trying to acquire new users, than it is to be losing money, because it costs so much to service existing users. The latter signals a bad business model, at least for the moment, whereas the former offers a semblance of hope.

- Fixed versus Variable Costs: For mature companies with established business models, it is better to have a more flexible cost structure (with more variable costs and less fixed costs). With money-losing, high-growth companies, the reverse is true, since it is the fixed cost portion that yields economies of scale, as the company grows.

b. Growth: Repeating a value nostrum, growth is not always value-creating and not all growth is created equal.

- Existing versus New Users: A user-based model, where you can grow cash flows from existing users is more valuable, other things remaining equal, than a user-based model that is dependent on adding new users for growth. The reason is simple. Since a company already has expended resources to get existing users, any added revenue it derives from them is more likely to flow directly to the bottom line. Adding new users is more expensive, partly because it costs money to acquire them, but also because new users may not be as active or lucrative as existing ones.

- Cost of New User Acquisition: This is a corollary of the first proposition, since the value of a new user is net of user acquisition costs. Consequently, user-based companies that are more cost-efficient in adding new users will be worth more than user-based companies that spend considerable amounts on promotion on marketing, to the same end.

This contrast is best illustrated by looking at Netflix and Spotify, both subscriber-based companies, but with very different models for paying for content. Netflix pays for content as a fixed cost, and derives economies of scale, when it adds fresh subscribers, whereas Spotify pays for content, based upon how much subscribers listen to songs, making it a variable and existing user based cost. As a result, Netflix derives much higher value from both existing and new subscribers:

| Netflix | Spotify | |

|---|---|---|

| Number of Subscribers | 117.6 | 71 |

| Annual Revenue/Subscriber | $ 113.16 | $ 77.63 |

| Subscriber Service Expenses (as %) | 18.90% | 79.24% |

| CAGR in subscriber count | 223.93% | 369.86% |

| Value per Existing Subscriber | $ 508.89 | $ 108.65 |

| Cost of acquiring New Subscriber | $ 111.01 | $ 27.30 |

| Value per New Subscriber | $ 397.88 | $ 81.35 |

| Value of all Existing Subscribers | $ 59,845.86 | $ 7,714.28 |

| + Value of all New Subscribers | $ 137,276.49 | $ 20,764.56 |

| - Corporate Cost Drag | $ 111,251.70 | $ 13,139.75 |

| =Value of Operating Assets | $ 85,870.65 | $ 15,339.10 |

c. Revenue Models: There are three user-based models, the first is the subscription-based model (that Netflix uses), the second is the advertising-based model (that Yelp uses) and the third is a transaction-based model (that Uber uses). There are companies that use hybrid versions, with Amazon Prime (membership fees and incremental sales) and Spotify (Subscription plus Advertising) being good examples. Each model comes with its pluses and minuses.

- Subscription models tend to be stickier (making revenues more predictable) but they offer less upside potential (it is difficult to grow subscription fees at high rates).

- Advertising models scale up faster, since they require little in capital investment and adding new users is easier (since they free), but revenues are heavily driven by user intensity (how much time you can get users to stay in your ecosystem) and exclusive data (collected in the course of usage).

- Transaction models are the riskiest, since they require users to use your product or service, but they also offer the most upside, since your upside is less constrained. Amazon Prime's value, in my view, does not stem primarily from the subscription revenues of $99/year but from Amazon's capacity to sell Prime members more products and services.

While no model dominates, picking the wrong revenue model can quickly handicap a business. For instance, using a subscription-based model for a transaction business, where usage varies widely across users, can result in self-selection, where the most intense users choose the subscription-based model to save money, and less intense users stay with a transaction-based model.

Differentiating across User-based Models

With the user-based framework in place, we can start distinguishing between user-based companies. Using existing user value and new customer acquisition costs as the dimensions, we can derive a matrix of companies that go from user-value stars to user-value dogs.

While the combination of high user value with low user acquisition costs may sound like a pipe dream, it is what network benefits and big data, if they exist, promise to deliver.

- Network benefits refer to the possibility that as you grow bigger, it becomes easier for you to get even bigger, making it less costly to acquire new users. That is the promise of ride sharing, for instance, where as a company gets a larger share of a ride sharing market, both drivers and customers are more likely to switch to it, the former, because they get more customers and the latter, because they find rides more quickly.

- Big data, in a value framework, offers user-based companies an advantage, since what you learn about your users can be used to either sell them more products or services (if you are a transaction-based company), charge them higher premiums (if you are subscription-based) or direct advertising more effectively (if advertising-based).

Many user-based companies aspire to have network benefits and to use data well, but only a few succeed.

The Pricing Game

As I look at user-based companies, some of which are being priced at billions of dollars, I am struck by how few of them are built to be long term businesses and how many of them are being priced on user numbers and buzz words. Using the framework from the last section, I would like to develop some common features that bad user-businesses seems to share in common and use one high profile examples, MoviePass , to make my case.

Mediocre User-based Companies

Given that so many young companies market themselves, based upon user and subscriber numbers, and that some of them can become valuable companies, are there signs that you can look for that separate the good from the mediocre companies? I think so, and here are a few red flags:

- All about users, all the time: If the entire sales pitch that a company makes to investors is about its user or subscriber numbers, rather than its operating results (revenues and operating profits/losses), it is a dangerous sign. While large user numbers are a positive, it requires a business model to convert these users into revenues and profits, and that business model will not develop spontaneously. Companies that do not work on developing viable business models go bankrupt with lots of users.

- Opacity about user data: It is ironic that companies that market themselves to investors, based upon user numbers, are often opaque about key dimensions on users, including renewal (churn) rates, user behavior and side costs related to users. The companies that are most opaque are often the ones that have user models that are not sustainable.

- Bad business models: If having no business model to convert users to operating results is a bad sign, it is an even worse sign when you have a business model that is designed to deliver losses, not only in its current form, but with no light at the end of the tunnel. That is usually the consequence of having losses that scale up as the company gets bigger, because there are economies of scale.

- Loose talk about data: The fall back for many user based companies that cannot defend their business models is that they will find a way to use the data that they will collect from their users to make money in the future (from targeted advertising or additional products and services), without any serious attempt to explain why the data will give them an edge.

- And externalities: Many user based companies argue that their "innovative" twists on an existing business will both expand and alter the business, leading to benefits for other players in that business, who, in turn, will share their benefits with the user based companies.

MoviePass: Too Good to be True?

If you subscribe to MoviePass, for a monthly subscription of $10, you get to watch one theatrical movie, every day, for the entire month. Given that the average price of a theater ticket in the US is $9, this sounds like an insanely good deal, and for an avid movie goer, it is, and the service had two million subscribers in May 2018. MoviePass, though, pays the theaters for the tickets, creating a model that is more designed to drive it into bankruptcy than to deliver profits.

When confronted by the insanity of the business model, Mitch Lowe, the CEO of MoviePass, argued that after an initial burst, where subscribers would see four or five movies a month, they would settle into watching a movie a month, allowing the service to break even. Since Mr. Lowe is a co-founder of Netflix and a former CEO of Redbox, I will concede that he knows a lot more about the movie business than I do, but this is an absurd rationale. If the only way that your service can become viable is if people don't use it very much, it is not much of a service to begin with.

In its early days, MoviePass seemed to be trying to build a viable business model, and acquired some high profile venture capital investors, but it was eventually acquired by Helios and Matheson, a data analytics firm, in a transaction in August 2017. It is Helios and Matheson, intent on giving both data and analysis a bad name, that instituted the $10 a month for a movie-a-day subscription. The subscription worked in delivering users but it, not surprisingly, came with large losses. As MoviePass has continued to burn cash (more than $20 million a month by April 2018), the share price of Helios and Matheson has collapsed, in a belated recognition of its non-viable business model.

|

| MoviePass Economics |

In its early days, MoviePass seemed to be trying to build a viable business model, and acquired some high profile venture capital investors, but it was eventually acquired by Helios and Matheson, a data analytics firm, in a transaction in August 2017. It is Helios and Matheson, intent on giving both data and analysis a bad name, that instituted the $10 a month for a movie-a-day subscription. The subscription worked in delivering users but it, not surprisingly, came with large losses. As MoviePass has continued to burn cash (more than $20 million a month by April 2018), the share price of Helios and Matheson has collapsed, in a belated recognition of its non-viable business model.

Adding to the sense that no one in this company has a grip on reality, Ted Farnsworth, the CEO of Helios and Matheson, argued that the service would continue and had acquired a $300 million line of credit. Since his backing for this line of credit was that he could issue the remaining authorized shares at the current market price, this indicates either extreme ignorance (potential equity issues don't comprise a line of credit) or unalloyed deception, neither of which is a quality that builds trust. Along the way, there have been other attempts to rationalize the model, including the possibility of using the data collected from subscribers to target advertising and the sharing of additional revenues generated by theaters and studios from more movie going. There is nothing exclusive about the data that will be collected from MoviePass subscribers and it is unlikely that theaters and small studios, already on the brink financially, will be willing to share their revenues. In short, this is a bad business model hurtling to a bad end, and the only question is why it took so long.

The Bottom Line

To build a good user-based business, you have to start with the common sense recognition that users are not the end game, but a means to an end. Unfortunately, as long as venture capitalists and investors reward companies with high pricing, based just upon user count, we will encourage the building of bad businesses with lots of users and no pathways to becoming successful businesses.

YouTube Video

Paper on User Based Value

Blog Posts on User-based Value

0 comments:

Post a Comment