West Ham’s 2014/15 season was like the proverbial game of two halves under Sam Allardyce, as a promising start took the club into the top four at Christmas, before a wretched slump produced just three victories in the next 21 games.

The Hammers still finished in a comfortable 12th place, which should presumably have satisfied joint chairman David Sullivan, as he described “retaining our Premier League status” as one of his highlights of the season. The club also qualified for Europe for the first time since 2007, albeit only by finishing top of the Fair Play table.

Nevertheless, they decided not to renew the manager’s contract, bringing in former player Slaven Bilic as Big Sam’s replacement in June. The Croatian has put together a very decent squad and already has wins against Arsenal, Liverpool, Manchester City and Chelsea under his belt. On the other hand, his team has also lost against Leicester City, Bournemouth and Watford.

Be that as it may, these are exciting times at West Ham, as the club is investing a lot of money in new players and will move to the £700 million Olympic Stadium in Stratford next season after 112 years at the Boleyn Ground.

"Slaven to the Rhythm"

The stadium move could revolutionise the club and is an amazingly good deal for the Hammers. The basic facts are that West Ham have a 99-year lease on the stadium starting from June 2016 and will pay just £15 million towards the conversion costs, which they can easily cover from the proceeds of selling Upton Park to property developer Gaillard Homes.

The stadium has a 54,000 capacity, around 19,000 more than the club’s current 35,000 seats, so will bring in substantially more money. The financial gains will be even more impressive, considering that West Ham will only pay annual rent of £2 to £2.5 million, while the running costs will be covered by the taxpayer.

Unsurprisingly, many have criticised this arrangement, though West Ham has argued that it has at least avoided the kind of “white elephants” seen in former Olympic host cities such as Barcelona, Athens and Beijing.

"A new royal family, a wild nobility"

Indeed, the club has mounted a vigorous defence: “Without us the stadium would lose money. West Ham make a substantial capital contribution towards the conversion works of a stadium on top of a multi-million pound annual usage fee, a share of food and catering sales, plus provide extra value to the naming rights agreement. Our presence underwrites the multi-use legacy of the stadium and our contribution alone will pay back more than the cost of building and converting the stadium over the course of our tenancy.”

On the other hand, it is worth noting that the deal is more favourable to the club than the one agreed with Manchester City in similar circumstances. They pay all the overheads on top of £4 million rent for the Etihad Stadium, which was funded by the taxpayer for the 2002 Commonwealth Games. Along the same lines, Chelsea and Tottenham would have to pay £10-15 million a year for using Wembley Stadium while their grounds are being developed.

Little wonder that Chris Bryant, the Shadow Secretary of State for Culture, Media and Sport described the deal as “astoundingly good” for West Ham, even though it will be a jolt for many fans to leave Upton Park with all its memories and fantastic atmosphere. The new stadium is in an excellent location, just minutes from Canary Wharf and the City and close to the Westfield shopping centre with very good transport links and infrastructure.

As vice-chairman Karren Brady said, “Our new home will be one of the greatest arenas in world football and a platform to transform the future of our great club.”

There is little doubt that this move will provide a major boost to the club’s finances, though these have steadily improved in the last two seasons in any case with West Ham reporting record revenue and another profit in 2014/15, though profit was down £7 million from £10 million to £3 million.

Revenue rose 5% (£6 million) from £115 million to £121 million, largely on the back of £3.6 million more TV money, though the other revenues streams also grew, albeit not much: commercial up 9% (£1.9 million) to £22 million and match receipts up 2% (£0.4 million) to £20 million. Player sales also increased by £2 million to £3 million.

On the other hand, costs grew at a faster rate: wages increased by 14% (£9 million) from £64 million to £73 million; player amortisation was up 20% (£4 million) to £22 million; and other expenses rose 11% (£2 million).

Of course, these days most clubs in the Premier League should make money, given the spectacular increases in the TV deals, allied with the restrictions on wage growth imposed by Financial Fair Play (FFP). In fact, only five of the 20 clubs in the top flight made a loss in 2013/14, the last season when all clubs have published their accounts.

Three of the five clubs that have so far reported their 2014/15 figures have registered lower profits, though only Manchester United actually lost money, due to their failure to qualify for Europe. This may well be a similar story at other clubs, as this is the second year of the current three-year TV deal, thus restricting revenue growth, while player costs are still rising.

A football club’s profitability can be very much influenced by profits on player sales, as can be seen in 2014/15 with Southampton making £44 million, manly due to the sales of Adam Lallana and Dejan Lovren to Liverpool plus Calum Chambers to Arsenal. The previous season saw Tottenham Hotspur make an amazing £104 million (largely due to the mega sale of Gareth Bale to Real Madrid), Chelsea £65 million (David Luiz to Paris Saint-Germain) and Everton £28 million (Marouane Fellaini to Manchester United).

Even though West Ham’s profit from this activity increased in 2014/15, it was still only £3 million, which could either be considered as implying that they are not a selling club (a good thing) or an indictment of their player development (a bad thing).

An additional £25 million from player sales would make a big difference to the bottom line, but it’s not going to happen in 2015/16 when the only sale of note was Stewart Downing to Middlesbrough for £5.5 million, while many players left on free transfers: Jussi Jaaskelainen, Modibo Maiga, Guy Demel, Carlton Cole and Kevin Nolan.

Even so, West Ham have managed to make profits in the last two years, which is a major improvement, considering that before 2013/14 they lost money seven years in a row, amounting to aggregate losses of £144 million.

In fairness, the small £4 million loss in 2012/13 already represented a step in the right direction, as the club had been averaging £23 million annual losses before then. This is a sign of the greater financial stability that the majority owners, David Sullivan and David Gold, have brought to the club since taking over in 2010.

To underline how little impact player sales have had on West Ham’s figures, this activity has only contributed £37 million to West Ham’s profits in the last nine years, i.e. less than Southampton made in the 2014/15 season alone. You have to go back as far as 2008 (£16 million) and 2009 (£22 million) for any meaningful profits from transferring players. In fact, West Ham have only averaged £1.4 million from player sales over the last four seasons, while actually contriving to lose £8 million in 2011.

The good news is that West Ham’s figures are no longer being hit by exceptional charges, which have had a major adverse impact on their accounts, adding up to £58 million since 2007.

The most notable charge was the £32 million they had to pay for breaching Premier League rules when acquiring Carlos Tevez and Javier Mascherano. They have also shelled out £10 million compensation for loss of office and £6 million following the termination of Dean Ashton’s contract due to severe injury.

It is worth exploring how football clubs account for transfers, as it has a major impact on reported profits. The fundamental point is that when a club purchases a player the costs are spread over a few years, but any profit made from selling players is immediately booked to the accounts.

So, when a club buys a player, it does not show the full transfer fee in the accounts in that year, but writes-down the cost (evenly) over the length of the player’s contract. Therefore, if West Ham spent £25 million on a new player with a 5-year contract, the annual expense would be only £5 million (£25 million divided by 5 years) in player amortisation (on top of wages).

However, when that player is sold, the club reports straight away the profit on player sales, which is essentially sales proceeds less any remaining value in the accounts. In our example, if the player were to be sold 3 years later for £32 million, the cash profit would be £7 million (£32 million less £25 million), but the accounting profit would be higher at £22 million, as the club would have already booked £15 million of amortisation (3 years at £5 million).

This is all horribly tedious, but it does help explain how clubs can spend big in the transfer market with relatively little immediate impact on their reported profits. Even though the annual cost of purchasing players is therefore somewhat reduced in the profit and loss account, it is worth noting that the impact of West Ham’s increasing spend in the transfer market has pushed up player amortisation, which has more than doubled from £10 million in 2012 to £22 million in 2015.

Obviously this is nowhere near as much as the really big spenders like Manchester United (£100 million), Chelsea (£72 million) and Manchester City (£70 million), but it is still worth keeping an eye on in future years.

The other side of the coin here is that all these signings have helped strengthen the balance sheet with player values (reported as intangible assets) climbing to £55 million, compared to only £15 million just four years ago. So what, you might say, but it is obviously good for any club to have better quality “assets” on the pitch.

That said, West Ham still have net liabilities (assets less liabilities) of £47 million, though this has improved by £4 million in the last 12 months.

Given all the accounting complexities arising from player trading, clubs often looks at EBITDA (Earnings Before Interest, Taxation, Depreciation and Amortisation) for a better understanding of how profitable they are from their core business. In West Ham’s case, EBITDA has recovered from negative £8 million in 2012 to £28 million in 2015, though it did fall back from £33 million the previous season.

This is not too bad, but at the same time helps to outline the challenge for clubs like West Ham, as the EBITDA at the leading clubs is significantly higher, despite their larger wage bills: Manchester United £120 million, Manchester City £83 million, Arsenal £64 million, Liverpool £53 million and Chelsea £51 million.

Since 2009, West Ham’s revenue has grown by 59% (£45 million) from £76 million to £121 million. The majority of this growth is down to TV money, which rose £35 million (79%) from £44 million to £79 million, though commercial income did grow £8 million (53%) from £14 million to £22 million and match day was up £2 million (13%) from £18 million to £20 million.

The highest increase within commercial came from retail and merchandising, which has risen 95% from £3.7 million to £7.3 million, partly due to the decision to bring the online retail business in house in 2012.

The impact of promotion from the Championship is evident from the £75 million increase since 2012 with all revenue streams benefiting from being in the Premier League.

Despite this significant growth, West Ham’s revenue of £121 million is still a lot lower than the Premier League elite, e.g. the top four clubs all earn more than £300 million: Manchester United £395 million, Manchester City £352 million, Arsenal £329 million and Chelsea £320 million.

West Ham are very much mid-table in revenue terms in the Premier League (10th highest the previous season) around the same level as Everton, Aston Villa and Southampton. Although the Hammers 2014/15 revenue growth of 5% was not as high as the previous season, this is very largely linked to the cycle of the TV deal. As last season was only the second year of the current three-year TV deal, it is unlikely that any club will see significant revenue gains in 2014/15.

However, West Ham’s revenue is now the 21st highest in the world according to the Deloitte Money League, ahead of famous clubs such as Marseille £109 million, AS Roma £107 million and Benfica £105 million.

This is basically due to TV money, which contributes nearly two-thirds (65%) of West Ham’s revenue. Commercial income and match receipts account for 18% and 17% respectively.

It is therefore no surprise that Brady has stated that retention of “our (Premier League) status in 2015/16 is an absolute necessity for the future wellbeing of our club.”

That might sound a little worrying, but it is a very similar story at other Premier League clubs. In fact, no fewer than 11 clubs had a higher reliance on TV money than West Ham in the 2013/14 season with Crystal Palace, Swansea City, Hull City and WBA all depending on TV for more than 80% of their revenue.

Considering the significance of Premier League television money to the Hammers, it is worth exploring how this is distributed in some detail. In 2014/15 their share rose 4% from £74 million to £76million. This is based on a fairly equitable distribution methodology with the top club (Chelsea) receiving £99 million, while the bottom club (QPR) got £65 million.

Most of the money is allocated equally to each club, which means 50% of the domestic rights (£22.0 million in 2014/15), 100% of the overseas rights (£27.8 million) and 100% of the commercial revenue (£4.4 million). However, merit payments (25% of domestic rights) are worth £1.2 million per place in the league table and facility fees (25% of domestic rights) depend on how many times each club is broadcast live.

In this way, West Ham were helped by climbing one place to 12th, but were held back by being broadcast live on one less occasion. However, they were still shown live 13 times, 4 more than Stoke City, which meant that they earned £2.2 million more (£11.0 million compared to £8.8 million), even though the club from the Potteries finished three places higher in the league.

My estimates suggest that West Ham’s 12th place would be worth an additional £35 million under the new contract, increasing the total received to an incredible £111 million. This is based on the contracted 70% increase in the domestic deal and an assumed 30% increase in the overseas deals (though this might be a bit conservative, given some of the deals announced to date). Of course, if West Ham could maintain their current 5th place, they would earn even more.

West Ham would also be targeting European qualification, which could bring in additional revenue, though their 2015/16 Europa League adventure will not generate much money, as they crashed out early to Romanian side Astra Giurgiu.

The Europa League is not a great money-spinner, unless you somehow manage to win the competition, but Everton did earn €7.5 million last season for reaching the last 16. The big money is obviously in the Champions League with English clubs averaging €39 million in 2014/15 and is getting higher, as the new TV deal from the 2015/16 season is worth an additional 40-50%, thanks to BT Sports paying more than Sky/ITV for live games.

This might feel like a somewhat unlikely ambition, but not if you listen to the two Davids. Gold said, “Realistically, in the next five years we would expect to be knocking on the door of Europe, The longer-term aim is to frighten the big boys of Chelsea, Manchester City, Manchester United, Arsenal and Liverpool. We want the big five to be looking over their shoulders.”

Stirring words, but they were echoed by Sullivan: “I’d love fourth now and we’d take our chances. I know it’s unlikely, but it really is possible.” His optimism is admirable, but he slightly ruined the effect when he started to talk of winning the Premier League and FA Cup double, “We’re very, very optimistic. I’m not talking it down. I want to talk it up. I believe it’s achievable. Look at what’s gone wrong with Chelsea – that looked an impossibility – so why shouldn’t the opposite happen to us?”

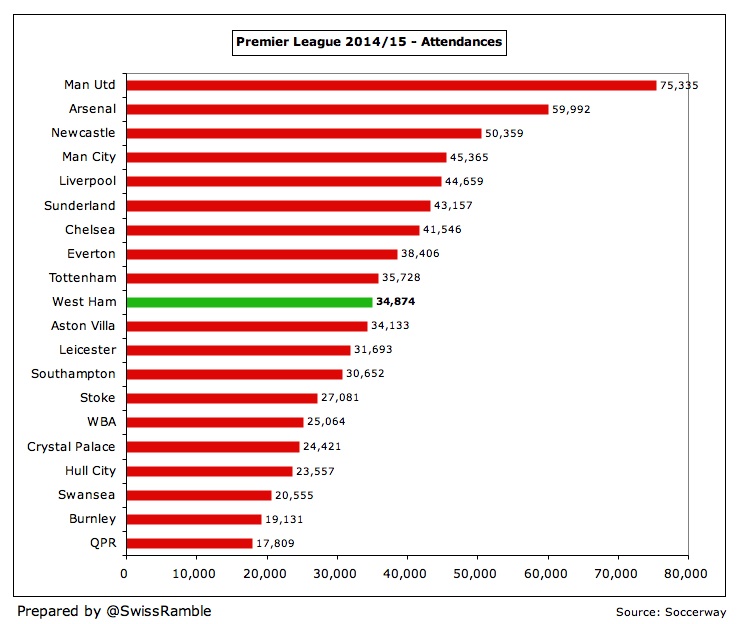

Match receipts rose 2.3% (£0.4 million) from £19.5 million to £19.9 million in 2014/15, even with one less home game (due to the run to the Carling Cup semi-final the previous season), as the average attendance rose 2.5% from 34,007 to 34,874.

West Ham supporters have lamented the club’s high ticket prices with the BBC Price of Football survey showing that 15 of the 20 Premier League clubs offered cheaper season tickets in 2014/15, despite prices being frozen that season. Even though the last season at Upton Park has seen a 5% price increase, season ticket sales for 2015/16 have exceeded 25,000, another club record.

The loyalty of the club’s fans is shown by attendances remaining at around the 34,000 level in the top flight, however well or badly the team has performed. The only slight blip came in the Championship in 2012, but the Hammers still averaged more than 30,000 in the second tier.

Nevertheless, West Ham’s match day revenue of £20 million is nowhere near Arsenal and Manchester United (both around £100 million), though a more valid comparison might be Tottenham, whose £44 million is more than twice as much.

This underlines the importance of the move to the Olympic Stadium, which should significantly increase West Ham’s revenue, not just because of the considerably larger capacity, but also the availability of more corporate hospitality and premium seats. Brady confirmed that only 200 of the 3,700 premium seats remained available.

The good news for fans is that many tickets in the new stadium will be sold at lower prices with thee cheapest season ticket being reduced to £289. While Brady was keen to link this to the benefits of the new broadcasting contract, others have pointed out that this is easier for West Ham than most, due to their extraordinarily generous stadium deal.

Commercial revenue rose 9% (£1.8 million) from £20.0 million to £21.8 million, comprising £14.6 million from commercial activities and £7.3 million from retail and merchandising.

Even though Brady proudly proclaimed that West Ham are “officially recognised as one of the world’s leading football brands by Brandfinance, placing us in the top 8 most valuable football brands in Premier League clubs and 16th overall in the world”, the fact remains that their commercial income pales into insignificance compared to heavyweights such as Manchester United, who generate £196 million from this activity.

That comparison might be a little unfair, but it is worth noting that Tottenham earned £42 million and Aston Villa and Newcastle United £26 million (in the 2013/14 season). Growth was a little disappointing, especially given that commercial and administrative staff rose from 136 to 164.

To be fair, the growth is sure to be better in the 2015/16 season, thanks to new sponsorship agreements. Less than a month after previous shirt sponsor Alpari went out of business, West Ham signed a three-year deal with online bookmaker Betway worth £20 million. This is worth £6.7 million a year, so more than double the £3 million that Alpari were paying.

Similarly, a new five-year kit supplier deal was signed with Umbro, which is reportedly worth twice as much as the previous deal with Adidas, which was valued at an estimated £2 million.

Given the higher profile afforded by the Olympic Stadium, the move should deliver plenty of commercial opportunities with the board noting that the club is already “receiving approaches from big brands that are desperate to be part of our exciting journey.” Furthermore, the new club megastore with 12,000 sq ft will be three times as large as the current club shop. In time, this should be reflected in much higher commercial income.

Wages rose 14% (£9 million) from £64 million to £73 million, despite players, management and training staff falling from 100 to 93, leading to the wages to turnover ratio worsening from 56% to 60%. Since the first season back in the Premier League in 2013, wages and revenue have both grown at a similar rate: wages by (29%) £17 million and revenue by (34%) £31 million.

The wage bill will be inflated by having four reasonably high-profile players on loan (Alex Song, Carl Jenkinson, Victor Moses and Manuel Lanzini), while it will also be impacted by extending the contracts of some players (Diafra Sakho, Aaron Cresswell and Winston Reid).

The amount paid to the highest paid director, believed to be Brady, was virtually unchanged at £646,000.

Although West Ham’s wages to turnover ratio increased, it is still the second best the club has recorded in the last seven years and much better than the 90% suffered in the Championship. It is also well within the standard achieved in the Premier League with 13 of the 20 clubs grouped in a fairly narrow range of 56-64% the previous season.

West Ham’s wage bill of £64 million was only the 13th highest in the 2013/14 season, exactly in line with their league placing. Even though this has increased to £73 million, to place this into context, it is only around a third of the elite clubs, who all pay around £200 million: Manchester United £203 million, Manchester City £194 million, Chelsea £193 million and Arsenal £192 million.

Nevertheless there is a clear bunching of clubs in the £60-70 million range, as the traditional bigger spenders like Newcastle United, West Ham and Aston Villa have only grown a little, while the nouveaux riches like WBA, Stoke City, Swansea City and Southampton have all had to significantly increase their wage bill in order to compete.

It is worth noting that West Ham’s wage bill has only risen by 8% since 2008, while others have grown much faster, e.g. Stoke City 411%, Southampton 362% and WBA 211%.

Sullivan did warn that the club would be restricted by FFP, following the big spending this summer: “As a result, we are now at the maximum wages we are allowed to pay under Premier League rules and, therefore, if we wanted to buy again in January we would no doubt have to sell someone before we would be allowed to make signings. It also means we expect the club to make a loss of between £10m and £17m this year, depending on where we finish in the Premier League and the number of games we have televised. This is indicative of just how seriously we took this window and the signings we wanted to make.”

This has been reflected in “major investment in the first team squad of £32.5 million (2014/15) and £42.0 million (2015/16)”. Last season saw the arrivals of Mauro Zarate, Enner Valencia, Aaron Cresswell, Cheikou Kouyate, Diafra Sakho, Diego Poyet and Morgan Amalfitano. Subsequent to the latest accounts, the club invested in Pedro Obiang, Dimitri Payet, Angelo Ogbonna, Michail Antonio, Nikica Jelavic, Stephen Hendrie and Darren Randolph.

Although reported transfer figures are notoriously unreliable, it is clear that there has been a major ramping up of expenditure in the four seasons following promotion. In that period, West Ham have a net spend of £93 million, averaging £23 million a year, compared to just £3 million in the preceding six years.

In fact, over that four-year period, West Ham were the 6th highest net spenders in the Premier League, only beaten by the usual suspects: Manchester United, Manchester City, Chelsea, Liverpool and Arsenal.

This is all driven by the club’s desire to maximise the chances of staying in the Premier League until the move to the Olympic Stadium. As Sullivan said, “I cannot remember a more exciting or successful window during our time at the club. We brought in 12 new players at a cost of over £40m, but that was only possible because David Gold and I made sure we dug deep to get the players we wanted. We thought it was important this season, with the move to the new stadium, that we bought players in every position to create the best squad and team that has been at the club since we arrived.”

Despite this spending spree, net debt actually fell £6.8 million from £73.5 million to £66.7 million with gross debt being cut by £2.5 million to £89.1 million and cash increasing by £4.3 million to £22.4 million. Around £49 million of the debt has put in by the owners, David Sullivan and David Gold, as unsecured shareholder loans – unchanged from the previous year. This represents over half of the club’s gross debt of £92 million, leaving £39 million of external debt and £0.6 million of debenture loans under the Hammers Bond Scheme.

External debt includes secured bank loans with interest charged at 3% to 3.75% over LIBOR, which have been refinanced until December 2016, though the club repaid £6.5 million on 31 August after the accounts were finalised. The club has also arranged additional short-term finance of £30 million with JGF Limited, secured on future income from the Premier League broadcasting contract, which is repayable in August 2016 and replaces the previous loan with the Vibrac Corporation. To date, £25 million of this facility has been drawn down.

"Diamond Smiles"

In addition to the financial debt, West Ham had £22 million of net transfer fees payable plus £9 million of contingent liabilities (dependent on the success of the football club or players making a certain number of club or international appearances). On top of that, there is a further net £37 million of transfer fees payable for players purchased after the accounts closed.

Furthermore, interest of 6-7% has been accrued on the owners’ loans, but is not paid or added to the loans until the loans are repaid, so there is another £9 million of potential debt “hidden” in accruals.

It is clear that West Ham are building up their debt in order to give themselves the best chance of success, both in terms of financial debt and transfer debt, though this is probably OK, so long as they avoid relegation.

In fairness to West Ham, there are seven clubs in the Premier League that owe more than them with five having debt above £100 million, namely Manchester United £411 million, Arsenal £234 million, Newcastle United £129 million, Liverpool £127 million and Aston Villa £104 million.

Moreover, the club has pledged to be free of external debt by the time it leaves the Boleyn Ground. The hope is that the proceeds from the sale of the Boleyn Ground to Galliard Homes will cover the Olympic Stadium £15 million conversion fee plus “some of our bank debt”.

According to the profit and loss account, West Ham’s net interest payable of around £6 million is one of the highest in the Premier League, albeit considerably lower than Manchester United £35 million and Arsenal £13 million. However, the cash payment is only £2 million, as the interest on the owners’ loans is not being paid.

West Ham’s improved finances are also reflected in the cash flow statement. Taking 2014/15 as an example, the club generated an impressive £43 million from operating activities, before spending £31 million on player registrations, investing £2 million in infrastructure and making £2 million of interest payments. They then made a net £2.5 million loan repayment, leaving a positive cash flow of £4 million.

This is indicative of the approach that Sullivan and Gold have taken since 2010, though they have not had to invest so much personally in the club in the last two years. In those six years, West Ham generated £69 million of cash from operating activities, which was supplemented by £75 million of financing from the owners (£49 million from loans and £26 million from an increase in share capital), giving £144 million of available funds.

Around two-thirds of this (£95 million) was spent on new players, £22 million on loan and interest payments and £8 million on capital expenditure. The remaining £20 million has served to increase the cash balance.

In line with the trend at other clubs, West Ham’s cash increased last year from £18 million to £22 million, though this is still a long way behind the leaders, e.g. Arsenal £228 million, Manchester United £156 million and Manchester City £75 million.

Sullivan and Gold now own 86.2% of the club and, though they have insisted that it is not for sale, West Ham is fast becoming an attractive investment opportunity. Indeed, last year they expressed a desire to sell some shares, valuing the club at £400 million.

Wealthy buyers will certainly be interested in purchasing a club of West Ham’s history in an iconic new stadium with massive potential to grow attendances, match day income and commercial revenue. There are a lot of parallels with Manchester City with the added advantage that the Hammers are not only located in London, but in an area that has already received an influx of foreign investment with Qatar purchasing the Olympic Village and China pouring money into the Docklands.

"Handy Andy"

If the club is sold following the move to Stratford, some of the profits would be returned to the taxpayer, but it is not clear what proportion. The only potential fly in the ointment would be if the club had to pay compensation if their move were deemed to contravene European state aid laws.

The other appeal to investors is FFP, especially as UEFA have recently relaxed the regulations for new owners, who will now be allowed to make larger losses, as long as they can produce a business plan that will show how they will reach break-even. This modified stance is a move from “austerity to sustainable growth” in an effort to encourage investment into European football.

"Don't Look Back in Anger"

West Ham are firmly in favour of FFP, according to Brady: “FFP is the legislation which, for the next season at least, will limit the ability of clubs to over-extend themselves on players’ costs and will likely enable all clubs, including ourselves, to increase profitability, and we continue to operate within the rules. We are hopeful that FFP will continue in some form in the next broadcast deal.”

As it stands, West Ham are arguably now one of the most exciting “projects” in European football. Whatever the rights and wrongs of the Olympic Stadium deal, it is difficult to disagree with Brady, when she says that it will be a “game changer for West Ham”. The challenge will be to advance into this brave new world, while retaining the characteristics of what Slave Bilic described as “a cult club”.

{kind=link}