As Arsenal enter the business end of the season, there is still much to play for, even though they are now likely to be eliminated from the Champions League by the mighty Barcelona. The domestic double is still up for grabs with nobody running away with the league, while the Gunners’ recent record in the FA Cup is second to none. However, many supporters are nervous about the team’s ability to finish the job, as the customary spate of injuries has led to a distinct dip in form.

The club’s wonderfully named chairman, Sir Chips Keswick, is keeping the faith: “This has been an unpredictable Premier League season thus far. What is important is that we are in contention and I am sure that we have the resources and ability within the squad to sustain a strong challenge.”

However, the club has not really strengthened the squad in the last two transfer windows. In the summer, they were the only Premier League club not to buy an outfield player, though the arrival of top-class goalkeeper Petr Cech has been an undoubted success. It was much the same in January when Arsenal only signed Egyptian midfielder Mohamed Elneny from Basel.

The fans’ frustration that the club has not fully utilised its spending power has once again been underlined by the publication of Arsenal’s financial results for the six months up to 30 November 2015, which revealed hefty cash balances of £159 million.

This is in line with the £162 million cash at the same time last year, but is lower than the £228 million reported in the annual accounts as at 30 May 2015. This is nothing to worry about, as this is simply due to the usual phasing of cash inflows and outflows with most of a football club’s income coming in the second half of the season. In particular, most season ticket renewals are paid in April and May, so Arsenal’s cash balance will always be at its highest when the annual accounts are prepared.

That said, the current £159 million cash balance is still one of the highest Arsenal have had in their interim accounts: 2011 £115 million, 2012 £123 million, 2013 £143 million and 2014 £162 million.

Everything else being equal, Arsenal’s cash balance will again be significantly higher when the next set of annual accounts is released. Depending on when transfer fee stage payments come due, it should be around the £225-250 million level.

Unsurprisingly, Arsenal have more cash than any other club in world football. Although not every Premier League club has published its accounts for the 2014/15 season, the North London side is clearly in a class of its own with the closet challengers being Manchester United, though their £156 million was still £72 million lower than their London rivals, followed by Manchester City £75 million.

It’s a similar story with the leading continental clubs, all of whom held significantly lower cash than Arsenal in 2015: Real Madrid £84 million, Bayern Munich £78 million, Barcelona £58 million and Juventus £5 million.

While it is advisable to put some money aside for a rainy day, there would have to be a monsoon of biblical proportions to justify Arsenal’s current cash levels. At the end of the 2013/14 season, they actually held 40% of the entire Premier League cash balances. However, the relative value of this cash is diminishing, as other mid-tier clubs are now benefitting from the influx of TV funds, e.g. Crystal Palace and Stoke City have £29 million and £26 million respectively.

Clearly Arsenal have been spending money. In fact, in the last six months the club had a net cash outflow of £69 million, even though they basically only broke-even on operating activities (after adding back non-cash expenditure on player amortisation and depreciation and adjusting for working capital movements). They then spent a net £39 million on player registrations (purchases £47 million less sales £8 million), largely due to stage payments from previous transfers.

They also invested £10 million in infrastructure improvements, notably substantial redevelopment at the London Colney training centre and Youth Academy at Hale End, plus some Emirates enhancements such as LED floodlights.

A further £14 million went on servicing the outstanding debt (loan repayment £8 million, interest £6 million), which is worth remembering whenever any ill informed amateur starts spouting nonsense about Arsenal’s debt being fully repaid. There was also a £5 million corporation tax payment, being the balance of the tax bill on the 2014/15 profits.

It is worth highlighting that Arsenal generated positive cash inflows of around £65 million in the second half of each of the last two seasons to turn around the outflows of the first half of the season, e.g. 2014/15 had a net outflow of £46 million at the interims, but this was converted into a net inflow of £20 million by the end of the year.

"I still haven't found what I'm looking for"

Of course, the raw figure in the accounts is a bit misleading, as not all of this cash balance is available to spend on transfers. Once more, for the cheap seats: not all of the cash balance represents a transfer fund.

In the face of growing criticism, chief executive Ivan Gazidis has emphasised this point: “It is quite untrue that we are sitting on a huge cash pile for some unspecified reason. The vast majority of that cash is accounted for in various ways.”

In fact, the club is so sensitive on this point that last year’s annual accounts noted that “proper consideration” of the cash balance should make deductions for the debt service reserve and the net amount owed on previous player purchases.

The irritating debt service reserve has been required ever since the 2006 bond agreements, though it does raise the question of whether these arrangements could be renegotiated given Arsenal’s significantly better financial position today, thus freeing up this money (£23 million in these accounts, £35 million for the full year).

"Genius of Love"

Like every other football club, Arsenal have not paid all the cash upfront for transfer fees, but have (sensibly) agreed stage payments, so part of the cash balance has to be reserved to pay sums due on those transfers. This has been reduced by £20 million following settlements of some transfer liabilities, but it still stands at £45 million.

As a good economist, manager Arsene Wenger has explained that the club’s relatively low spending is due more to supply and demand than an unwillingness to spend: “It is not a shortage of money, just a shortage of players”, adding that there was “quantity, not quality” in the transfer market. He has a point; though it is disappointing that Arsenal’s scouting network has failed to identify a few decent (available) players somewhere in world football that could improve the squad.

It might be difficult to find value in the market, especially as the prices quoted to Arsenal and other leading English clubs tend to be higher than those for continental clubs, with sellers clearly being aware of the wealth coming from the Premier League TV deals. This may be a little reminiscent of Harry Enfield’s “I saw you coming” sketch, but that’s the reality of the football market today. Clubs like Arsenal need to blow the other clubs out of the water – or there’s simply no point having more money.

"How was it for you?"

The other problem with hoarding cash was noted by no less a person than Sir Chips Keswick, when he spoke of the forthcoming blockbuster Premier League TV deal: “the increased revenues will also very likely bring with them inflationary pressures in terms of both the wage bill and the transfer market.” Exactly – so why not splash the cash before then?

This is exacerbated by, of all things, Brexit, as the Pound has depreciated by around 10% against the Euro in the last few months, thus reducing the spending capacity of English clubs abroad.

Despite all of these factors, there is still substantial money available to spend. It’s clearly not as much as the figure in the books, but we can say with some conviction that Arsenal should have around £100 million to spend in the summer on improving the squad.

Nonetheless, it should be acknowledged that Arsenal have been spending more in the transfer market in the past few seasons. For example, it might come as a surprise to Arsenal fans that they have the third highest net spend in the Premier League over the past three seasons of £111 million (according to Transfer League), only behind Manchester City £241 million and Manchester United £199 million.

In that period, the club has brought in Mesut Ozil, Alexis Sanchez, Danny Welbeck, Calum Chambers, Gabriel and Mathieu Debuchy, though it is somewhat strange that they have only spent a net £13 million this season on Cech and Elneny.

Arsenal did report a small £3 million loss after tax for the latest interims, compared to a £6 million profit for the same period the previous season. They were actually boosted by a £3 million tax credit, due to the revaluation of deferred tax balances based on the UK’s lower future rates of corporation tax. Before tax, Arsenal suffered a £12 million deterioration, as a £6 million profit swung into a £6 million loss.

By far the biggest reason for this decline was profit on player sales, as the club made hardly any money from this activity, compared to £27 million last season, mainly due to the sales of Thomas Vermaelen to Barcelona and Carlos Vela to Real Sociedad.

As a counterpoint, Arsenal’s underlying profitability actually increased with EBITDA (Earnings Before Interest, Taxation, Depreciation and Amortisation) rising from £23 million to £35 million.

This was because revenue grew by £10 million (6%) from £148 million to £158 million, mainly due to broadcasting, up £7 million (14%) to £60 million, thanks to higher UEFA Champions League distributions. There was also growth in commercial income, up £3 million (5%) to £55 million, and player loans, £1 million higher at £1.5 million. On the other hand, match day revenue was £2 million (4%) lower at £41 million, due to fewer home matches being played.

Expenses (including wages) were £2 million lower, but player amortisation rose £4 million to £29 million.

"Hector was the first of the gang"

There was limited activity in the property business, with the only transaction of note being recognition of the final instalment of the sale of Queensland Road development, though revenue and profit were both £2 million higher.

The accounts also benefited from a £5 million reduction in net finance charges from £12 million to £7 million, thanks to the introduction of Financial Reporting Standard (FRS) 102. Although this had minimal impact on this year’s profit, it has meant a restatement of prior year comparatives.

In particular, the interest rate swap, used to fix the interest rate on the floating rate stadium bonds, has to be included on the balance sheet at fair value with any changes in value reported in the profit and loss of each period. As there was a significant increase in negative fair value last year, with the financial markets anticipating that UK interest rates would remain lower for longer than previously expected, this meant a higher charge.

Of course, Arsenal have been very much the poster child of the Premier League in terms of making money. In fact, you have to go back as far as 2002 to find the last time that they made a loss. They have made total combined profits before tax of £226 million in the eight years since 2008.

The question is whether this year’s loss at the interim stage will mark a change in this positive trend? It seems unlikely, given that Arsenal have been in a similar position twice recently, namely in 2011 and 2014, when they managed to convert a first half loss into a full year profit on both occasions.

Nevertheless, these accounts again show how much influence player sales (and property development) have had at Arsenal. Excluding these items, Arsenal have actually lost money in each of the last five seasons.

More encouragingly, Arsenal’s underlying profitability was actually better in these interims compared to last year, as they would have reported a smaller loss after excluding these once-off factors: £8 million in 2015/16 compared to £21 million in 2014/15.

Actually, stability in the playing squad with no major sales might be considered as “a positive factor for the club”, according to Sir Chips. The good news is that Arsenal no longer need to sell players from a financial perspective.

The only other English club that has published half-year accounts is Manchester United and it is interesting to compare the Red Devils with Arsenal, as this highlights one major difference between the two. United made a £33 million profit before tax, which was £39 million better than Arsenal’s £6 million loss, even though their costs were £48 million higher.

The main reason for United’s superiority is their commercial revenue of £137 million, which is an incredible £82 million more than Arsenal’s £55 million. Match day revenue is also £14 million higher, but that is misleading, as United have played six more home games in the period than Arsenal.

Nevertheless, Arsenal have the seventh highest revenue in the world, based on 2014/15 annual accounts, having overtaken Chelsea last season. This is obviously pretty impressive, but the harsh reality is that they are still a fair way behind the leading elite, e.g. at £331 million they are around £100 million lower than the two Spanish giants, Real Madrid £439 million and Barcelona £427 million.

If we compare Arsenal’s revenue with the other clubs in the Deloitte Money League top ten, it is immediately apparent where their biggest problem lies, namely commercial income. Arsenal’s £103 million might not seem so bad, but it is only higher than Juventus, and is lower than every other club at this level.

Granted, the £123 million shortfall against PSG (£103 million vs. £226 million) is largely due to the French club’s “friendly” agreement with the Qatar Tourist Authority, but there are still major gaps to the other clubs in commercial terms: Bayern Munich £108 million, Manchester United £97 million, Real Madrid £85 million, Barcelona £82 million and Manchester City £71 million.

On the plus side, Arsenal enjoy the highest match day income in the world, while they are also competitive on broadcasting revenue, only really losing out compared to the individual deals negotiated by Real Madrid and Barcelona.

Arsenal’s commercial revenue passed £100 million for the first time in 2014/15, as it shot up £26 million (34%) from £77 million to £103 million, largely due to the new PUMA kit deal, which started in July 2014.

Looking at previous years, we can see that usually the full year commercial revenue is more or less double the first half. On that basis, we could estimate Arsenal’s 2015/16 revenue as £110 million (i.e. twice £55 million).

Although the chairman described the interim increase of £2.8 million (5%) as “robust growth”, his comments last year seemed more appropriate: “Inevitably, this growth rate will now slow as we have our key partnerships with Emirates and PUMA in place for the medium term.”

Even though Arsenal had the highest percentage growth since 2012 of the leading six English clubs, the reality is that they are still a long way below the Manchester clubs: United’s 2014/15 revenue was up to £197 million (nearly twice as much), while City’s revenue was £173 million. That might be to be expected, but less understandable is that Arsenal are also behind Liverpool £116 million and Chelsea £108 million.

Despite an increase in the number of worldwide partnerships to 33, the concern is that Arsenal’s commercial performance will continue to place them at a competitive disadvantage relative to other leading clubs. Further substantial increases are only likely to come as a result of success on the pitch, which again makes you wonder why the available cash has not been spent on strengthening the squad.

Although match day income fell in the interims, this was because Arsenal played two less home games (9 compared to 11) this season, so it should be made up in the rest of the year. Match day revenue is always weighted towards the second half, so my expectation is that Arsenal will again top £100 million by the end of the season. The actual amount will depend on the number of home games, i.e. progress in the cup competitions.

Incidentally, Arsenal have confirmed that there will be no general increase in ticket prices next season.

Similarly, broadcasting income is always higher in the second half of the year, though the actual amount received will depend on Arsenal’s final Premier League position and how far they progress in the knockout competitions.

Each place in the Premier League is worth an additional £1.2 million, while the amount received also depends on the number of Arsenal games broadcast live, though the vast majority of the payment is based on an equal distribution among the 20 clubs: half the domestic payment, 100% of the overseas payment and commercial income.

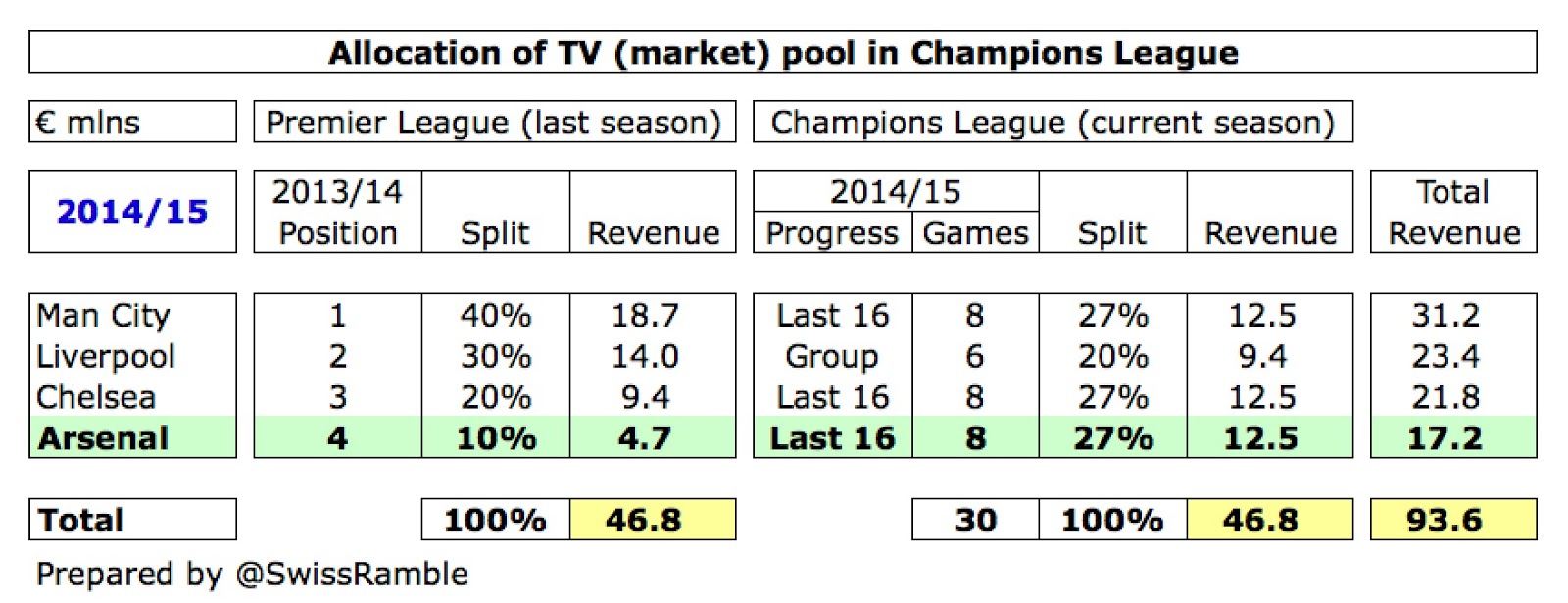

However, Arsenal will earn more from the Champions League, as the prize money has increased in the first year of a new three-year UEFA revenue cycle, e.g. €12 million for group participation (compared to €8.6 million), €1.5 million for a group stage win (€1 million), €5.5 million for reaching the last 16 (€3.5 million).

The market pool is also significantly higher, thanks to BT Sports paying more than Sky/ITV for live games. Arsenal’s 2015/16 payment will partly depend on how far they progress in this season’s Champions League, but also how well the other English clubs do, so if City and Chelsea get past the last 16, Arsenal will receive a smaller share for this element than 2014/15.

However, the other half of the market pool is based on where they finished in the previous season’s Premier League (3rd in 2014/15, compared to 4th the year before), which means that their share here will increase from 10% to 20%.

Unfortunately, Arsenal do not disclose their wage bill in the interim accounts, but they do include some comments that suggest that it was around the same level as the previous year. On the one hand, there was no Champions League qualification bonus in this year’s figures, as the 2014/15 accounts included the players’ bonus earned as a result of finishing in third place. On the other hand, the chairman stated, “This has been offset by increases in the underlying wage bill arising from certain contract extensions within the squad”, (e.g. Santi Cazorla and Theo Walcott).

What is interesting is how the wage bills at the top clubs have been converging around the £200 million level. Arsenal’s £192 million is still the 4th highest, but the gap has been closing. Chelsea once again have the highest wage bill in the top flight at £216 million, which is the first time since 2010, ahead of Manchester United £203 million and Manchester City £194 million.

Both Manchester clubs actually saw a reduction in wages in 2014/15. United’s decrease was due to their lack of success on the pitch, as bonuses fell, while City’s is partly due to a group restructure, where some staff are now paid by group companies, which then charge the club for services provided.

Continued investment in the playing squad has seen a further increase in player amortisation to £29 million, up £4 million (14%). On a full year basis, this has risen from just £22 million in 2011 to £54 million in 2015, and is likely to be higher still in 2016.

As a reminder, player amortisation is the way in which player purchases are reflected in the profit and loss account. To illustrate how this works, if Arsenal paid £25 million for a new player with a five-year contract, the annual expense would only be £5 million (£25 million divided by 5 years) in player amortisation (on top of wages).

As might be expected, those clubs who have traditionally spent big in the transfer market have the highest player amortisation: Manchester United £100 million, Manchester City £70 million and Chelsea £69 million.

There is no mention of whether the interims include another payment to the company of majority owner Stan Kroenke. This has amounted to £3 million in each of the last two years for a “wide range of services”, albeit with precious little transparency about exactly what these services comprised.

Gross debt has reduced by £2 million from £234 million to £232 million with net debt virtually unchanged at £72 million, due to a similar decrease in cash from £161 million to £159 million.

Arsenal’s debt comprises long-term bonds that represent the “mortgage” on the stadium (£194 million), debentures held by supporters (£14 million) and derivative financial instruments (£24 million). The club has no short-term debt to worry about.

Prior year debt figures have also been restated following the implementation of FRS 102, so the debt as at 31 May increased from £234 million to £239 million.

Although Arsenal’s debt has come down significantly from the £411 million peak in 2008, it is still a heavy burden, requiring an annual payment of around £19 million, covering interest and repayment of the principal. The interest payable of £13 million is a lot more than any other Premier League club (£5-6 million at Manchester City, Everton, West Ham and Liverpool) with the exception of Manchester United, who leapt to £35 million in 2014/15.

Although the net debt stands at only £72 million, thanks to those large cash balances, the gross debt of £232 million remains the second highest in the Premier League, only behind Manchester United, who still have £444 million of debt even after all the Glazers’ various re-financings.

Overall, it feels a little like Groundhog Day at Arsenal. To paraphrase the late, very great David Bowie, “The film is a saddening bore, for we’ve lived it ten times or more.”

While Arsenal might not be at the very pinnacle of football clubs financially, they are still better placed than most, so it is difficult to understand why the club has not used all of its resources to give itself the best chance of success. Very few fans want the club to throw caution to the winds, but they could surely invest more than they have done.

By most standards, Arsenal have a fine squad that is certainly capable of challenging for major honours, but in recent years there has always been something lacking. The latest financial figures continue to demonstrate that there is enough money to be competitive in the market.

Who knows whether a couple of world class recruits would make the difference and take the club to the next level, but surely it would be better for the club to spend what it can, so that its wealth can be seen on the pitch rather than gather dust in the accounts.